If you want to avoid the high volatility of the stock market but find the low returns of traditional bank savings accounts or Certificates of Deposit (CDs) disappointing, bonds may very well emerge as the absolute protagonist of the financial market in the second half of 2026. As the high interest rates observed as of June begin their full-fledged downward cycle in the latter half of the year, bonds—which were once considered the exclusive playground of giant institutional players—are firmly establishing themselves as an essential portfolio asset for individual retail investors. In this post, we reveal the 2026 bond investment trends chosen by smart investors aiming to capture both tax efficiency and capital gains simultaneously in the global capital markets.

Bond investment is not overly complicated. To put it simply, it is a type of financial certificate where you lend money to a sovereign government (like the US Treasury) or a corporation, and in return, you receive fixed interest payments (coupons) alongside the structural rights stipulated by that security.

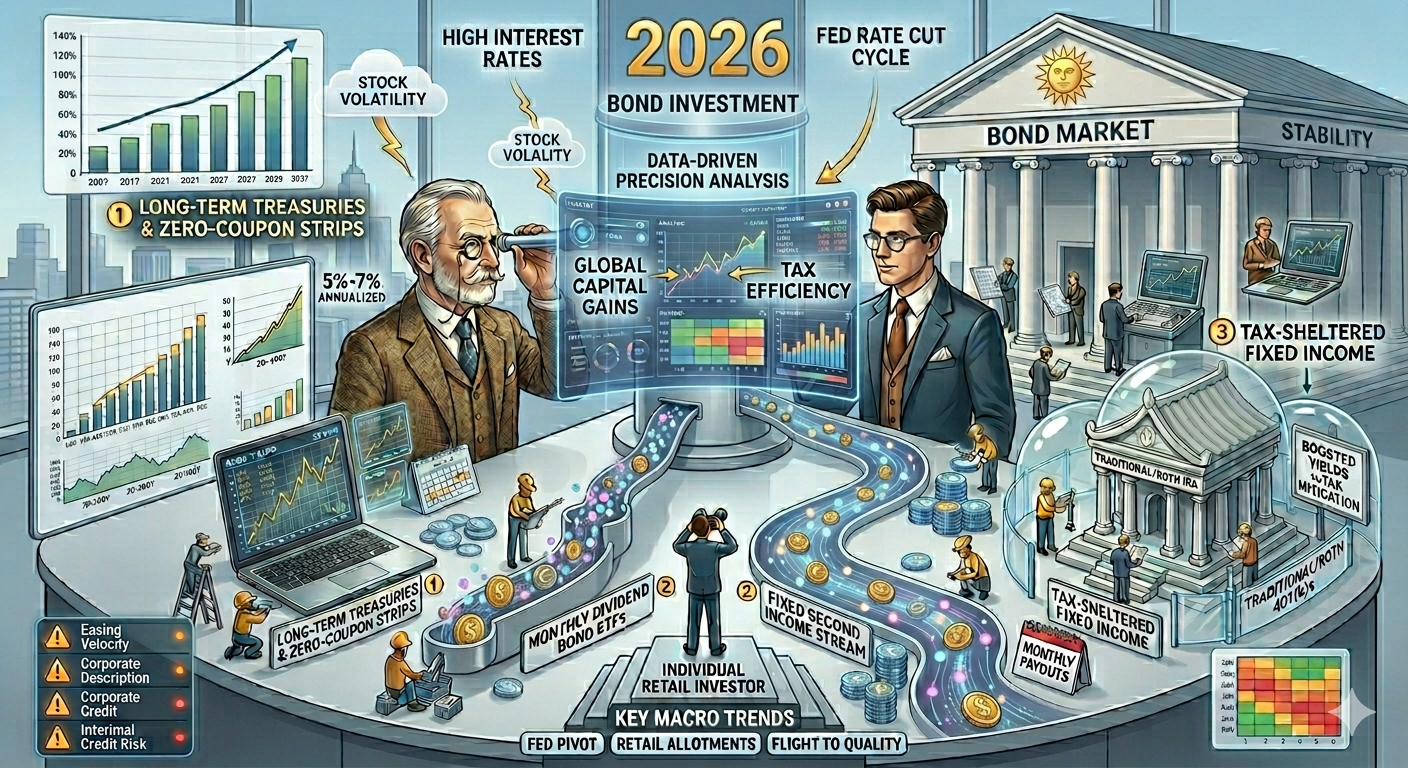

1. Introduction: Why Bonds Right Now? (The Window of Opportunity)

As of June 2026, the US stock market has experienced significant upward momentum, driven heavily by booms in core sectors like artificial intelligence and semiconductors, leading major indices to hit historic milestones. Globally, even amidst geopolitical tensions and macroeconomic shifts that have kept the US Dollar Index remarkably strong and interest rates stubbornly elevated, a structural shift is on the horizon. As these geopolitical conflicts show signs of cooling down and moving toward stability, global economic growth is expected to moderate.

Consequently, inflation will stabilize back toward the Federal Reserve’s target levels, and interest rates will enter a long-term downward stabilization phase. As the Federal Reserve paves the way for a clear cycle of benchmark fed funds rate cuts, a major wealth-generation window is opening up—one that relies entirely on the foundational economic principle that when interest rates fall, bond prices rise.

2. Three Macro Trends Driving the 2026 US Bond Market

- The Fed’s Late-2026 Pivot: Wall Street consensus indicates that the Federal Reserve will safely engineer an initial “insurance cut” in late 2026 (around Q4) once inflation sustainably prints near target. This macroeconomic backdrop means the second half of 2026 is the absolute cyclical bottom to aggressively accumulate long-duration Treasuries before the floodgates of institutional capital open.

- Surge in Retail Treasury Allotments: The US Treasury has optimized access for individual investors, expanding the ease of direct purchases for Treasury bills, notes, and bonds through institutional and retail platforms. Crucially, the yields on long-term tranches, such as the 10-year and 30-year maturities, present an incredibly attractive entry point before the easing cycle accelerates.

- Global Flight to Quality: Amidst structural realignments in European and Asian capital markets, the influx of global foreign capital tracking US fixed income acts as a powerful catalyst. The massive global demand for US sovereign debt drastically reduces market volatility, reinforcing a highly stable, upward-trending environment for Treasury securities.

3. Three Dominate Bond Investment Vehicles Preferred by Investors

Active market capital is currently concentrating into three distinct asset types, highly dependent on the specific financial goals of the investor.

① Long-Term Treasuries and Zero-Coupon Strips: Maximizing Capital Gains

With the interest rate cut trajectory explicitly clear, the largest volume of retail capital is flowing directly into long-term bonds with extended durations. There is a particularly sharp increase in preference for Treasury Strips (Separate Trading of Registered Interest and Principal of Securities), which separate the principal and interest components into independently tradable zero-coupon securities.

- Key Characteristics: Because a minor drop in market interest rates triggers a substantial percentage increase in the price of ultra-long bonds, this vehicle is highly favored by aggressive investors who care less about regular coupon payments and more about capturing massive capital gains from buying low and selling high.

- Popular Vehicles: 30-year US Treasury bonds, ultra-long-term US Treasury ETFs focusing on maturities of 20 years or more (such as TLT), and leveraged duration products for sophisticated traders.

② Monthly Dividend Bond ETFs: Generating a Fixed Second Income Stream

Passive income generation has become a massive trend not only for retirees but also for millennial and Gen Z investors looking to hedge their equity exposure. Consequently, monthly distribution bond ETFs have completely taken over the retail market.

- Key Characteristics: Utilizing high-quality investment-grade corporate bonds or liquid high-yield debt as their underlying assets, these funds distribute consistent payouts yielding roughly 5% to 7% annualized on a monthly basis. They provide critical psychological defense during equity market corrections by ensuring consistent, non-correlated cash flow.

- Popular Vehicles: Monthly-dividend US Aggregate Bond ETFs (such as BND or AGG), and diversified liquid ETFs targeting investment-grade corporate bonds rated investment grade or higher.

③ Tax-Sheltered Fixed Income: Boosting Yields via Traditional/Roth IRAs and 401(k)s

Given that modern retail investors are hyper-focused on their net returns, utilizing tax-advantaged accounts for fixed-income positioning has moved from a niche secret to standard practice.

- Key Characteristics: Purchasing taxable bond ETFs inside a traditional IRA, Roth IRA, or 401(k) allows investors to completely defer or eliminate ordinary income taxation on interest coupons. This shift effectively increases the net portfolio yield by a significant margin compared to executing the exact same trades in a standard taxable brokerage account, where coupons are taxed at ordinary income rates.

- Recent Trend Line: A popular strategy in 2026 involves allocating long-term high-yield corporate bonds or long-term Treasuries directly into a Roth IRA, holding them through the rate-cut cycle, and utilizing tax-free growth to maximize wealth compounding.

4. Comprehensive Strategy Matrix by Investor Persona

| Investment Type | Primary Target Group | Core Portfolio Objective | Structural Risk Level | Strategic Tactical Advice |

| Long-Term US Treasuries | Capital Growth Seekers | Lock in maximum capital gains as market yields fall | High Duration Risk | Highly lucrative when the pace of Federal Reserve rate cuts accelerates. |

| Monthly Dividend ETFs | Consistent Income Seekers | Generate steady, monthly cash flow and predictable coupon yields | Low to Moderate | Focus predominantly on liquid, high-grade corporate debt or aggregate indices. |

| Tax-Sheltered Fixed Income | Defensive Capital Preservers | Maximize tax mitigation and internal compound interest | Very Low | Utilizing specialized accounts like Traditional/Roth IRAs is mandatory to avoid coupon tax drag. |

5. Critical Caveats and Risk Management Guardrails

While the 2026 US bond market offers clear structural tailwinds, individual investors must navigate three distinct operational risks before committing capital:

- The Reality of Easing Velocity (2026 vs. 2027): While some Wall Street aggressive pivot-hopefuls expect a rapid decline, a more realistic macroeconomic view suggests that the consecutive rate-cutting cycle will likely manifest its full velocity in early 2027. If the Federal Reserve lowers interest rates at a much slower pace than expected due to sticky service-sector inflation, your investment capital will be locked into fixed-yield assets for an extended period, inducing severe opportunity cost.

- Corporate Credit Risk Management: When moving out of sovereign debt into corporate bonds, verifying credit ratings and corporate debt maturities is vital. Even in 2026, lingering refinancing risks remain concentrated around specific highly-leveraged corporate sectors, demanding extreme caution and strict reliance on investment-grade issuers.

- Interim Principal Loss Vulnerabilities: If a US Treasury bond is purchased directly and held all the way to its official maturity date, your principal is fundamentally guaranteed by the federal government. However, if you are forced to liquidate your bond ETF position prematurely on the secondary open market during a sudden, unexpected spike in market interest rates, you can absolutely suffer a net loss of principal.

6. Conclusion: Key Takeaways for Today’s Investors

Bonds are far from a boring, stagnant investment; rather, they represent one of the most scientific, predictable methods of converting the macroeconomic passage of time and central bank policy into structured portfolio returns.

- Mastering the Timing: Understand the difference between the 2026 bottoming and the 2027 easing. The second half of 2026 represents the accumulation phase where smart retail investors buy the rumor of rate cuts. Early 2027 will likely be the execution phase where the consecutive rate cuts materialize into clear capital appreciation.

- Shield Your Returns: For those actively designing a retirement timeline, channeling fixed-income assets through tax-deferred vehicles like IRAs or 401(k) accounts is the ultimate alpha strategy to secure both safety and tax minimization in 2026.

- Watch Macro Signals: Pay close attention to Federal Reserve dot plots, labor market data, and FOMC communication regarding inflation targets. The velocity of the upcoming interest rate cuts will dictate exactly how fast your long-term bond prices will appreciate.

AI Disclosure: Created in collaboration with Google Gemini. All core content was authored, reviewed, and edited by the author.