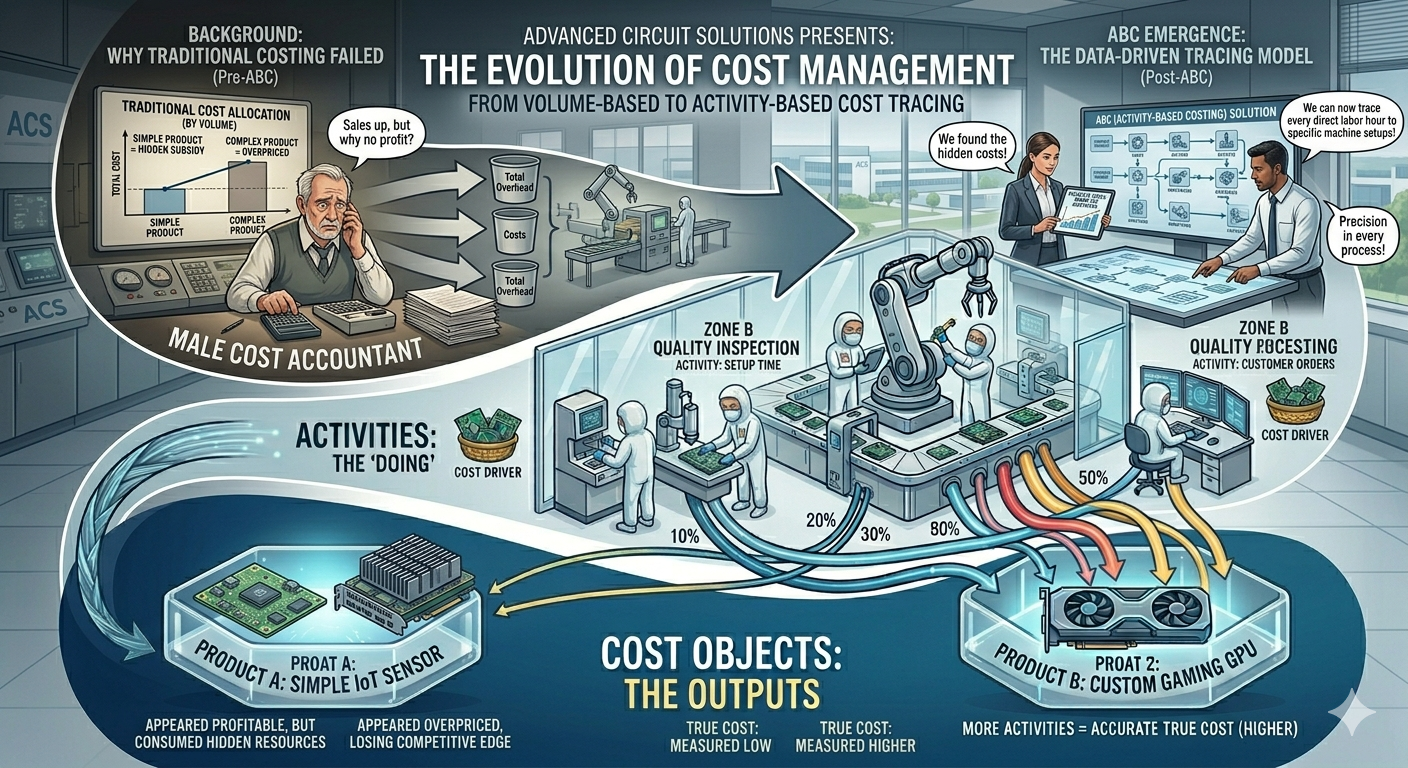

“We are selling more than ever, so why does it feel like we aren’t making any money?”

If you are a business owner, executive, or corporate strategist, this is a question that has likely kept you up at night. When revenues are climbing but net profit margins remain stubbornly stagnant, the root cause rarely lies with your sales team. Instead, the culprit is often a fundamental flaw in how you calculate and allocate your costs. In today’s complex corporate landscape, relying on outdated financial metrics can blind you to where your capital is actually leaking. To uncover these hidden drains, businesses are increasingly implementing Activity-Based Costing (ABC)—a precise accounting methodology designed to expose the true cost of operations in modern commerce.

1. Understanding ABC Through an Everyday Analogy: “The Fair Split vs. The Bad Split”

Before diving into the mathematical models, let’s look at a common scenario that perfectly mirrors corporate cost distortion: going out to dinner with a group of friends.

- The Traditional Approach (The Generic Split): Imagine three friends go to a restaurant, and the final bill comes out to $90. One friend orders an expensive filet mignon steak, while the other two order basic side salads. To keep things simple and avoid an awkward calculation, they decide to divide the bill evenly, splitting it three ways. Everyone pays $30. The friend who ate the steak walks away with a fantastic deal, while the friends who only had salads leave feeling frustrated and cheated. This is exactly how traditional accounting distorts corporate costs.

- The ABC Approach (The Itemized Split): Now, imagine the group looks closely at the itemized receipt. Instead of averaging the total, they ask: “Who performed the specific action of ordering the steak?” and “Who consumed the premium resources?” By tracking the direct cause and effect, the calculation shifts. The friend who ordered the steak pays $50, the friend who had the pasta pays $20, and the friend who had the salad pays $20. Ultimately, everyone pays precisely for the specific activities they initiated and the resources they consumed. This is the foundational logic of Activity-Based Costing.

2. What Exactly Does ABC Mean?

The acronym ABC is not just an arbitrary sequence of letters; it represents a highly logical, causal chain of cost assignment:

- Activity: First, management identifies the discrete operational actions required to deliver a product or service—such as resetting manufacturing machinery, conducting quality assurance checks, processing unique purchase orders, or executing data transfers.

- Based: Instead of assuming costs are driven by simple production volume, expenditures are allocated strictly based on how frequently and intensely these specific operational activities are performed.

- Costing: By linking resource consumption directly to these activities, the system calculates the accurate, distortion-free final cost and true profitability of an asset.

In the past, simply measuring direct labor hours was enough to estimate overhead. However, in a business environment characterized by automated processes and highly customized services, analyzing these discrete operational activities has become a prerequisite for corporate survival.

3. Traditional Accounting vs. ABC: Why Make the Switch?

Historically, when factories were packed with manual laborers rather than automated systems, a simple rule of thumb worked well: “If an employee spends more hours working on a product, that product naturally consumes more electricity and factory space.” In that environment, using direct labor hours as a blanket allocation base for overhead was highly reasonable.

- The Structural Shift in Manufacturing: Decades ago, labor hours directly correlated with overhead generation. Today, automated machinery, advanced software, and robotics have driven direct labor costs down significantly. Concurrently, indirect costs—such as software maintenance, complex system configurations, engineering modifications, and quality testing—have ballooned. Attempting to filter these massive, complex overhead pools through a single baseline like labor hours is no longer mathematically viable.

- The Trap of High-Volume Over-Allocation: When a company uses traditional volume-based drivers (like total units produced or direct labor hours) to distribute overhead, a dangerous distortion occurs. Simple, high-volume products that require very little administrative effort end up absorbing the vast majority of the company’s overhead costs. Meanwhile, low-volume, highly complex, and customized products—which demand constant machine reconfigurations, custom engineering, and heavy administrative oversight—appear artificially cheap. This cost distortion tricks executives into overpricing their core profitable products and underpricing their most expensive, resource-draining offerings.

- The Enablement via Information Technology: While the mathematical concepts behind ABC have been understood for decades, tracking thousands of micro-activities manually was once an administrative impossibility. Today, the exponential rise in computing power, real-time enterprise resource planning (ERP) systems, and cloud infrastructure allows corporate data platforms to seamlessly track, aggregate, and calculate complex activity drivers automatically.

4. Comprehensive Comparison: Traditional Costing vs. Activity-Based Costing

To optimize operational decision-making, it is vital to contrast how these two methodologies approach corporate data:

| Category | Traditional Costing | Activity-Based Costing (ABC) |

| Primary Allocation Base | Single, volume-based drivers (e.g., labor hours, machine hours) | Multiple, activity-based drivers (e.g., number of setups, inspection hours) |

| Cost Object Focus | Centered strictly around the final product or department | Centered around the discrete activities that consume resources |

| Data Precision | Low (Tends to over-allocate overhead to simple, high-volume assets) | High (Accurately reflects the actual resource footprint of each asset) |

| Core Objective | Standard financial reporting and external financial statements | Strategic management, pricing optimization, and process improvement |

| Real-World Analogy | Splitting a restaurant bill equally regardless of what individuals ordered | Paying an itemized bill strictly based on the exact items consumed |

5. Why ABC is Vital in the Modern AI and Automation Era

As advanced automation and artificial intelligence platforms redefine enterprise operations, traditional cost accounting has broken down entirely. When automated algorithms replace manual tasks, the primary driver of corporate expenditure shifts from human labor to technological infrastructure.

- The Explosion of Invisible Overhead: In automated systems, standard manual labor costs drop toward zero. Instead, the income statement is dominated by massive indirect expenses: cloud computing infrastructure, data centers, AI model training cycles, API usage fees, and ongoing algorithm maintenance. ABC prevents these costs from becoming a massive, unanalyzed overhead pool. It systematically breaks down cloud expenditures into specific operational activities—such as “Data Ingestion,” “Model Refinement,” and “Security Compliance”—giving executives clear insight into whether an automation project is genuinely driving a positive return on investment (ROI).

- Exposing the Real Cost of Hyper-Personalization: Modern companies frequently utilize machine learning to offer hyper-personalized corporate services. However, different clients require vastly different amounts of technical infrastructure. While a standard client might run entirely on a low-cost, off-the-shelf model, a premium enterprise client might demand continuous custom data processing and massive graphics processing unit (GPU) computing time. Traditional accounting averages these infrastructure costs across all accounts, obscuring profit margins. ABC tracks actual activity drivers, pinpointing exactly which clients are generating premium margins and which ones are quietly consuming your entire infrastructure budget.

Conclusion: Key Takeaways for Today’s Investors and Executives

Implementing Activity-Based Costing transforms financial data from a passive historical record into an active, strategic weapon for corporate optimization.

- Eliminate Profit Blind Spots: Moving away from standard volume-based allocations eliminates cost distortions, allowing you to identify products that seem profitable on paper but are actually destroying bottom-line value.

- Optimize Operational Processes: By mapping out expenditures to explicit activities, management can easily isolate non-value-added steps, allowing teams to streamline workflows, eliminate waste, and maximize margin efficiency.

- Navigate High-Tech Environments: In a corporate world dominated by cloud computing, automation, and AI infrastructure, tracking specific activity drivers is the only reliable way to measure the true ROI of technology investments and execute data-driven pricing strategies.

AI Disclosure: Created in collaboration with Google Gemini. All core content was authored, reviewed, and edited by the author.