While theoretical definitions are clear, a true leader’s skill lies in understanding how numbers actually move on the factory floor. Imagine a local bakery—specifically, a high-volume “Fish-bread” (Taiyaki) factory. The batter (direct materials) is poured into the molds at the very beginning of the process. However, the baking time (conversion costs) is incurred gradually as the product moves through the oven. By analyzing a simple example, we will explore how different accounting assumptions change the narrative and what these results signal to a savvy manager.

1. Setting the Scene: The Factory Data

Let’s look at the production data for our factory this month:

- Beginning Work-in-Process (WIP): 100 units (50% complete—these are the “half-baked” units from last month).

- Units Started this Period: 400 units (new batches entered into the oven this month).

- Units Completed & Transferred Out: 420 units (packaged and ready for sale).

- Ending WIP: 80 units (25% complete—remaining in the oven at month-end).

Cost Data for the Factory:

- Total Costs to Account For: $94,000

- Beginning WIP Cost: $10,000 (Materials: $6,000 / Conversion: $4,000)

- Current Period Costs: $84,000 (Materials: $44,000 / Conversion: $40,000)

- Key Condition: Materials are added 100% at the start of the process; conversion costs are added evenly throughout the process.

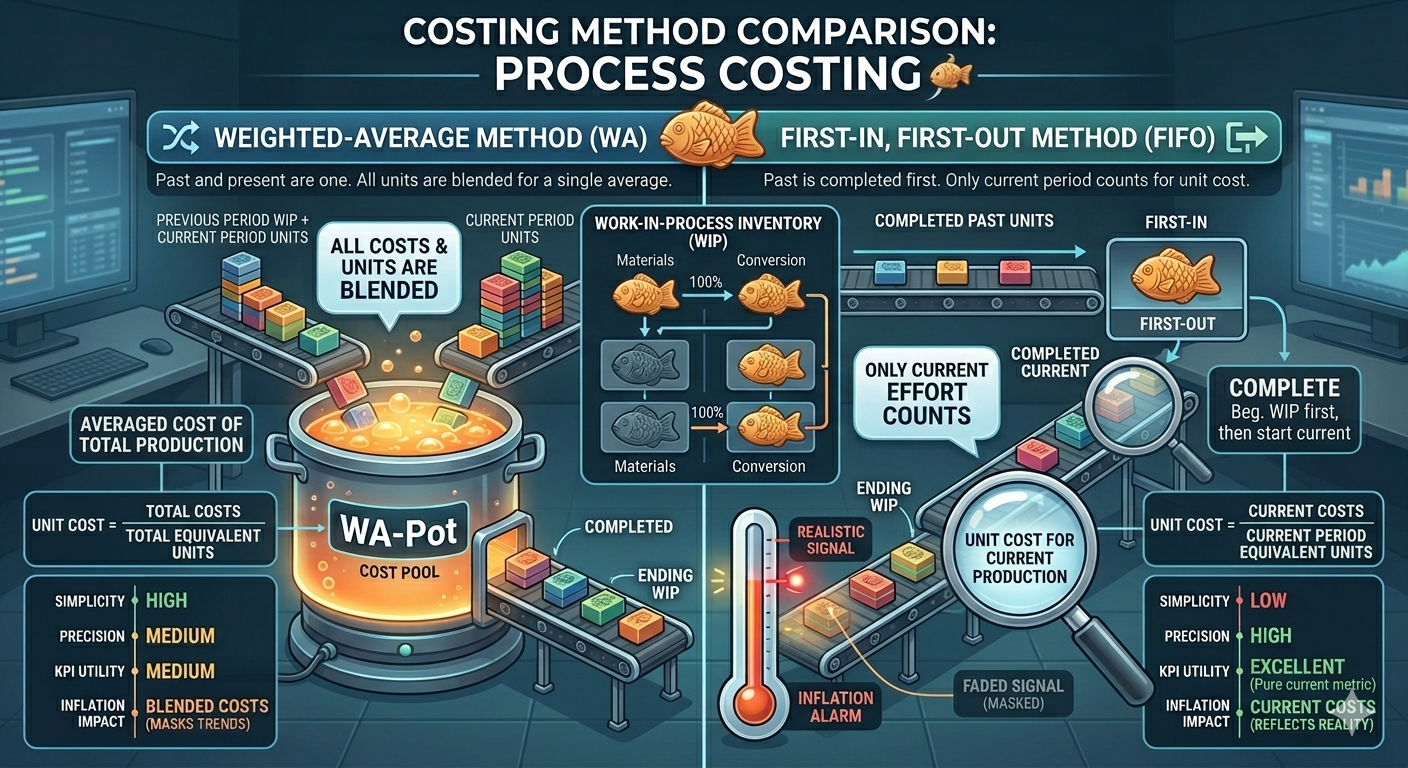

2. The Core Debate: Weighted-Average vs. FIFO

The fundamental difference between these two methods lies in how we treat the “ghosts of the past”—the beginning work-in-process.

| Category | Weighted-Average Method | FIFO (First-In, First-Out) |

| Logical Perspective | “The past and present are one.” All costs are blended into a single average. | “The past leaves first.” Prior units are finished first; unit costs are based only on current effort. |

| Equivalent Units (EUP) | Completed Units + Ending WIP Inventory | (Units Started & Completed) + Work to Finish Beg. WIP + Ending WIP |

| Cost Basis (Numerator) | Beg. WIP Costs + Current Period Costs | Only Current Period Costs |

| Managerial Utility | Simple to calculate; high practical convenience. | Measures pure efficiency for the current month (Superior KPI). |

| Inflation Impact | Blends in old, lower costs; makes current costs look lower. | Reflects current price hikes immediately; more realistic in volatile markets. |

3. Same Data, Different Reality

Even with identical physical data, the choice of “assumption” changes the denominator (EUP) and the numerator (Cost), leading to different strategic conclusions.

1) Comparison of Unit Costs

| Item | Category | Weighted-Average | FIFO | Notes |

| Equivalent Units | Materials | 500 units | 400 units | FIFO: (420-100) + 80 |

| Conversion | 440 units | 390 units | FIFO: (420-100) + (1000.5) + (800.25) | |

| Costs to Assign | Materials | $50,000 | $44,000 | FIFO ignores Beg. WIP costs in unit cost calc. |

| Conversion | $44,000 | $40,000 | FIFO focus on current month spending. | |

| Unit Cost | Materials | $100 | $110 | FIFO: $44,000 / 400 units |

| Conversion | $100 | Approx. $102.5 | FIFO: $40,000 / 390 units | |

| Total Unit Cost | $200 | $212.5 |

2) The Managerial Insight: Decoding the Gap

The table above reveals a critical truth for a business owner:

- Discovering the Cost Surge: Under the Weighted-Average method, the unit cost is $200. However, the FIFO method—which looks exclusively at this month’s performance—shows a cost of $212.5.

- Root Cause Analysis: This means either the price of flour (materials) has spiked ($100 → $110) or factory efficiency has dropped. The Weighted-Average method was masking this danger signal by blending it with cheaper costs from the previous month.

- Strategic Action: In an inflationary period, a manager must use the FIFO figure ($212.5) to re-evaluate product pricing. Relying on the blended average could lead to selling products at a hidden loss.

4. Business Implications

1) The Quality of Earnings: Avoiding the Illusion

Cost is not a fixed reality; it is a fluid number shaped by our assumptions.

- Detecting Profit Quality: While the Weighted-Average method might report a higher net income (due to lower blended costs), it doesn’t mean operational efficiency has improved. Managers must use FIFO to strip away the “illusion” of profit created by old, low-cost inventory.

- Asset Valuation: Ignoring the timing of material and conversion inputs leads to misvalued Ending WIP. This directly impacts the accuracy of the balance sheet.

2) Accountability: Separating the Past from the Present

The heart of management is “Responsibility Accounting.”

- Fair Performance Evaluation: It is unfair to judge a floor manager’s performance based on costs inherited from the previous month. FIFO provides a “pure effort” metric ($212.5), allowing for a fair KPI based on what the team actually controlled this month.

- Tracking Cost Drivers: If the FIFO cost jumps from $200 to $212.5, the manager can ask the right questions: “Did the raw material price increase, or did the baking time increase?” This question is the beginning of improvement.

3) Defensive Strategy in Inflation

In a volatile economy, your costing method becomes a survival strategy.

- Pricing Strategy: If you set your prices based on the $200 average, you will fail to cover the $212.5 required for current production. FIFO provides the strongest evidence for necessary price adjustments.

- Cash Flow Forecasting: When calculating the opportunity cost of capital tied up in inventory, using the most recent FIFO unit costs ensures a more accurate cash flow prediction.

Conclusion: Key Takeaways

- Weighted-Average is a stabilizer that smooths out fluctuations but can blind you to current trends.

- FIFO is a high-resolution lens that captures the “economic reality” of today’s production environment.

- Strategy: Use FIFO for internal performance evaluation and pricing, especially when material costs are rising. Use Weighted-Average only if the process is extremely stable and simplicity is the primary goal.

AI Disclosure: Created in collaboration with Google Gemini. All images and portions of the text were generated, reviewed, and edited by the author.