In a non-stop factory, products aren’t just “made”; they flow. The CEO’s challenge is: “How do we value units started last month but finished today?” Since we can’t track every cent to a specific bolt, we use Cost Flow Assumptions. Without these rules, profit manipulation and audit failures are inevitable.

1. Cost Flow Assumptions: Bringing Order to the Factory Floor

Imagine a massive food processing plant in Chicago or a semiconductor fab in Silicon Valley. The assembly lines never truly stop. Raw materials purchased at last month’s prices are sitting in half-finished units, while new materials bought at today’s rates are being poured in. This creates a classic managerial dilemma: “When a finished product rolls off the line, does it carry the cost of the old, expensive materials or the new, cheaper ones?”

In a high-volume environment—where thousands of identical units are produced—it is physically impossible to track every single cent back to a specific invoice. This is why we rely on Cost Flow Assumptions. These are not just accounting “tricks”; they are the logical rules we use to assign costs to products so that financial reporting remains consistent and objective.

The Dangers of Operating Without a System

Without a defined cost flow assumption, a company faces three major risks:

- Audit Nightmares: If costs are assigned randomly, auditors cannot verify the accuracy of the inventory value, leading to legal and financial repercussions.

- Profit Manipulation: A manager might be tempted to cherry-pick low-cost invoices during a bad month just to make the “bottom line” look better—a practice that distorts the true health of the business.

- Inconsistent Benchmarking: Without a steady rule, you cannot compare this month’s performance to the last. Your “unit cost” would fluctuate based on which receipt an accountant grabbed first, rather than the actual efficiency of the plant.

The Meeting of Past and Present

The biggest challenge in process costing is the Beginning Work-in-Process (WIP)—the items that were half-finished when the previous month ended.

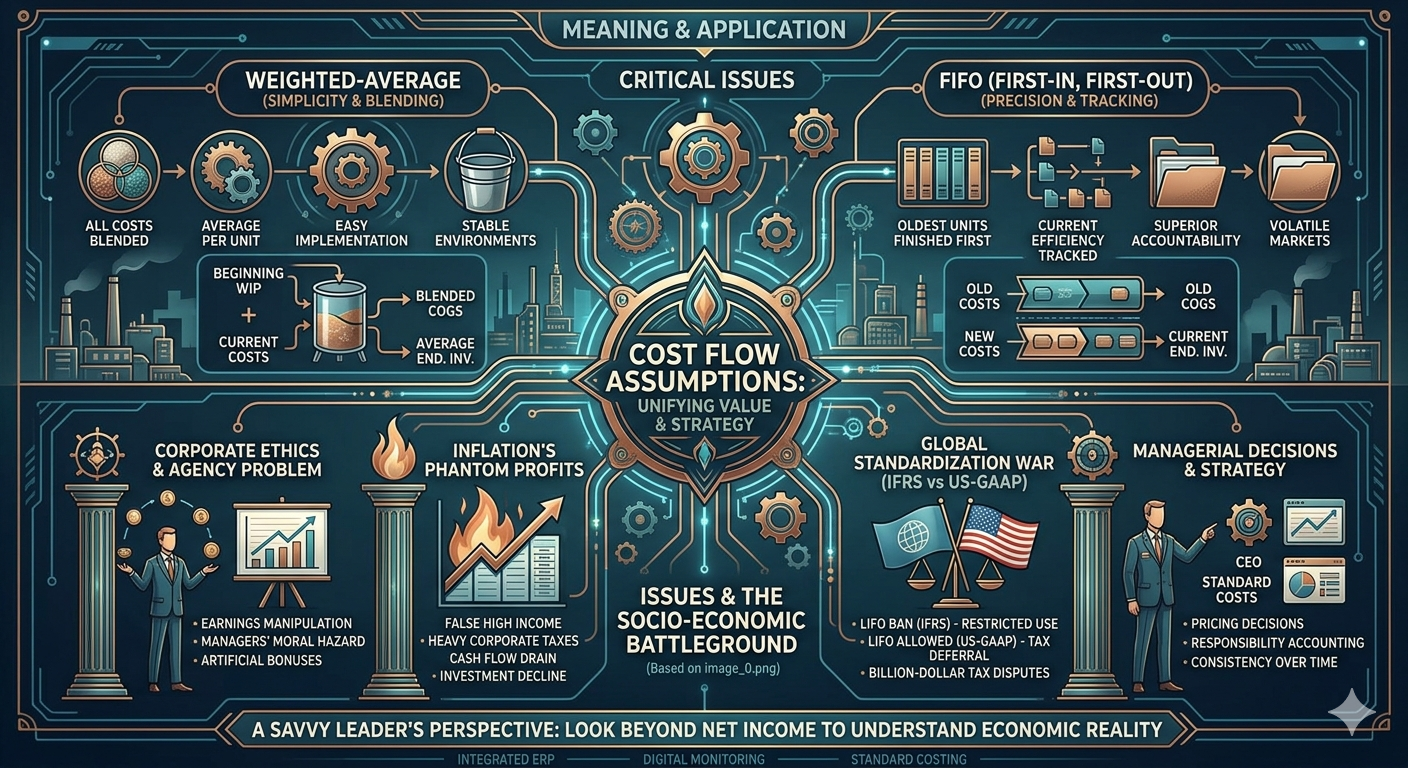

- The Weighted-Average Method treats the past and present as one single pool, blending them together.

- The FIFO (First-In, First-Out) Method draws a hard line between last month’s efforts and this month’s new production.

2. The Weighted-Average Method: The Power of Simplicity

The Weighted-Average method is built on a simple philosophy: “A widget is a widget.” It doesn’t matter if work started on a unit on Sunday night or Monday morning; all costs are thrown into one “bucket” and averaged out.

How the Math Works

To find the cost per unit, you take the total costs (Beginning WIP Cost + Current Period Costs) and divide them by the total equivalent units (Units Completed + Ending WIP Equivalent Units).

- The Advantage: It is incredibly easy to implement. It requires less record-keeping because you don’t need to know exactly how far along the beginning inventory was when the month started.

- The Drawback: It “muddies the water.” If inflation caused material prices to spike this month, that spike is diluted by the older, cheaper costs from last month. This makes it harder for a CEO to see exactly how efficient the factory was this month.

3. The FIFO Method: Precision for Performance Tracking

FIFO operates on the strict assumption that the oldest units (the ones already in the pipeline) must be finished and shipped out first. It keeps the “Old Costs” and “New Costs” in separate folders.

The Analytical Edge

In FIFO, we only use the Current Period Costs to calculate the current cost per equivalent unit. We assume the Beginning WIP was finished first using just a fraction of this month’s effort.

- The Advantage: This is a superior tool for Responsibility Accounting. It tells a manager exactly what it cost to produce something today, without the data being “contaminated” by what happened weeks ago. It is ideal for industries with high price volatility.

- The Drawback: It is complex. You must know the precise percentage of completion for the beginning inventory, which adds a layer of administrative burden.

4. Comparing the Engines: At a Glance

| Feature | Weighted-Average Method | FIFO Method |

| Core Logic | Blends old and new costs | Keeps old and new costs separate |

| Calculation | (Beg. Cost + Current Cost) / Total EU | Current Cost / Current Work EU |

| Simplicity | High (Easy to use) | Low (Requires more data) |

| Managerial Utility | Good for stable environments | Best for tracking current efficiency |

5. Strategic Pitfalls and Managerial Solutions

Choosing a method isn’t just about math; it’s about strategy. Here are the common traps and how a savvy leader avoids them:

The Inflation Trap

In periods of rising prices, the Weighted-Average method will result in a higher Cost of Goods Sold (COGS) than FIFO, potentially showing lower profits. Conversely, FIFO will show a “healthier” profit because it uses older, cheaper costs for the products sold. A leader must look beyond the profit number to understand which method is being used.

The “Garbage In, Garbage Out” Risk

Both methods rely on the “Percentage of Completion” for ending inventory. If a floor supervisor overestimates how finished the products are, the entire unit cost calculation breaks. This “contamination” can lead to poor pricing decisions and a false sense of security.

The Solution: Integrated Systems and Consistency

- Standard Costing Integration: Regardless of whether you use FIFO or Weighted-Average for reporting, you should compare the results against a “Standard Cost” (the ideal cost) to spot variances immediately.

- Digital Monitoring: Modern ERP (Enterprise Resource Planning) systems can track production in real-time, removing the “guesswork” from completion percentages and making FIFO as easy to manage as the Average method.

- The Rule of Consistency: Once you choose a method, you must stick with it. Changing methods frequently is a “red flag” to investors and tax authorities. Choose the model that best fits your production cycle and hold the line.

6. The Macro-Economic and Ethical Battleground

While cost flow assumptions seem like dry, internal accounting mechanics, they sit at the heart of intense debates involving corporate taxes, executive compensation, investor deception, and global economic policy.

Earnings Manipulation and the Agency Problem

Because changing a cost flow method can legally alter a company’s net income by millions of dollars, it creates a massive agency problem.

- Cherry-Picking for Bonuses: Many C-suite executives have bonuses tied directly to short-term net income or operating profit. In inflationary periods, using FIFO artificially inflates book profits (“paper profits”) without any actual operational improvement. Executives can reap massive performance bonuses based on accounting illusions rather than genuine innovation, leading to severe ethical dilemmas and moral hazard.

- Managing Expectations: Companies may deliberately manipulate production levels or inventory discharge pacing just to hit quarterly earnings targets, distorting the true economic health of the enterprise for Wall Street.

“Phantom Profits” and Tax Inequality under Inflation

During global supply chain disruptions and high-inflation cycles, the choice of cost flow assumptions becomes highly politicized.

- The Holding Gains Trap: Under FIFO, older, cheaper inventory is matched against current, inflated revenues. This yields high accounting profits, but these are “phantom profits.”

- The Cash Drainage Crisis: Governments tax these phantom profits at standard corporate rates. Consequently, after paying heavy taxes and shareholder dividends based on artificial profits, companies often lack the real cash required to replace their raw materials at today’s higher market prices. This drains corporate liquidity, which can trigger artificial economic slowdowns, reduced R&D, or preemptive layoffs.

The Global Standardization War (IFRS vs. US-GAAP)

The broader debate over cost flow rules has triggered geopolitical friction between international regulatory bodies.

- The Clash of Standards: International Financial Reporting Standards (IFRS), utilized by over 140 nations, strictly bans the Last-In, First-Out (LIFO) method, arguing that it misrepresents the physical flow of goods and serves primarily as a tax avoidance loophole. Conversely, US GAAP continues to permit LIFO, largely due to fierce lobbying from major American energy, chemical, and steel conglomerates.

- Billion-Dollar Tax Battles: If the United States were to fully align with global standards and abolish LIFO, American corporations would instantly face billions of dollars in retroactive corporate tax liabilities on accumulated inventory gains. Thus, cost flow assumptions are no longer just math—they are chess pieces in international tax diplomacy and lobbying warfare.

Conclusion: Key Takeaways

- Cost Flow Assumptions are essential logical frameworks that prevent accounting chaos and profit manipulation in mass production.

- Weighted-Average is best for businesses seeking simplicity and stability in their cost reporting.

- FIFO is the gold standard for CEOs who need to isolate current month performance and hold managers accountable for modern efficiency.

- The Big Picture: Cost flow assumptions ultimately dictate how corporate wealth is distributed among shareholders, executives, and the government. A truly savvy leader must look beyond the final net income figure and decode the socio-economic context of the underlying accounting framework.

AI Disclosure: Created in collaboration with Google Gemini. All core content was authored, reviewed, and edited by the author.