In our previous session, we examined the mechanism of “Job Order Costing.” We learned that since materials and time vary for each product, we use a “Predetermined Overhead Rate (POHR)” to estimate costs in advance. However, in the world of business, there is no such thing as a perfect prediction.

When you open the books at the end of the year and discover that the “Estimated Cost (Applied)” and the “Actual Money Spent” are different, what should you do? Today, we will compare the two key terms for this discrepancy: Overapplied and Underapplied overhead.

1. What Does “Apply” Mean? Coating the Product with Cost

In everyday English, “Apply” often means to “Apply for a job” or “Apply a rule.” However, in cost management, the word is much closer to the image of “spreading” or “coating.”

1) The Fundamental Image: “Coating the Surface”

When you put lotion on your face after washing or spread ointment on a wound, you say, “Apply the cream.”

- In Daily Life: Spreading cream evenly over the skin.

- In Accounting: The process of spreading Manufacturing Overhead (indirect costs) evenly over the surface of a “Job” (product). Common costs like electricity and rent aren’t visible in a specific product. Therefore, we set a benchmark (rate) and “apply” the cost to each product as it passes through the production line—Click, Click, Apply!

2) Underapplied: “Did we spread the ointment too thin?”

Here, Under- signifies “below the benchmark” or “insufficient.”

- Breakdown: Under (Insufficiently) + Applied (Coated/Allocated).

- The Scenario: You were supposed to cover the entire wound with ointment, but you used too little.

- Accounting Meaning: The actual electricity bill came to $1,000, but the cost “applied” to the products was only $800.

- Result: “We recorded less (Under) cost than reality! We need to add more expenses later.”

3) Overapplied: “The makeup is too thick!”

Conversely, Over- signifies “exceeding the benchmark” or “excessive.”

- Breakdown: Over (Excessively) + Applied (Coated/Allocated).

- The Scenario: You were supposed to apply makeup naturally, but you put on way too much, and it looks cakey.

- Accounting Meaning: The actual bill was $1,000, but because we applied overhead generously to every product, the total recorded was $1,200.

- Result: “We recorded more (Over) cost than reality! We need to reduce the expenses later to show the true profit.”

2. Why “Normal” Costing? Choosing Prediction Over Waiting

The concepts of application and variances are the heart of Normal Costing. While “Actual Costing” waits for all bills to arrive, the business world moves too fast for that. Managers choose Normal Costing because they cannot afford to wait for the utility company to send a bill.

1) The Definition: “A Strategic Mix”

Normal Costing doesn’t use actual figures for everything. Instead, it mixes “Actual” for direct costs and “Estimated” for indirect costs.

- Direct Materials & Labor: Use the Actual amount spent (since they are immediately visible).

- Manufacturing Overhead: Since the final bills aren’t available until year-end, we use a Predetermined Overhead Rate (POHR).

2) Why Use “Estimates”? (The Logic)

- Timeliness: If you wait for the December electricity bill, you won’t know the cost of a product made in June until January. Normal Costing allows you to calculate costs and set prices the moment a product is finished.

- Smoothing: Energy costs spike in the summer due to AC. If you used actual costs, products made in August would look more “expensive” than those made in May. Normal Costing applies an annual average rate to stabilize unit costs against seasonal spikes.

3) The 3-Step Process

- Step 1 (Beginning of Year): Forecast the total overhead and total activity (hours) for the year to set the POHR.

- Step 2 (During the Year): For every job, multiply [Actual Activity × POHR] to Apply cost. (This is your Applied Overhead).

- Step 3 (End of Year): Once the actual bills arrive, compare the “Applied Cost” with the “Actual Cost” and adjust the variance.

3. The Gap Between Forecast and Reality: Causes and Meanings

Understanding why the gap exists is the key to strategic management.

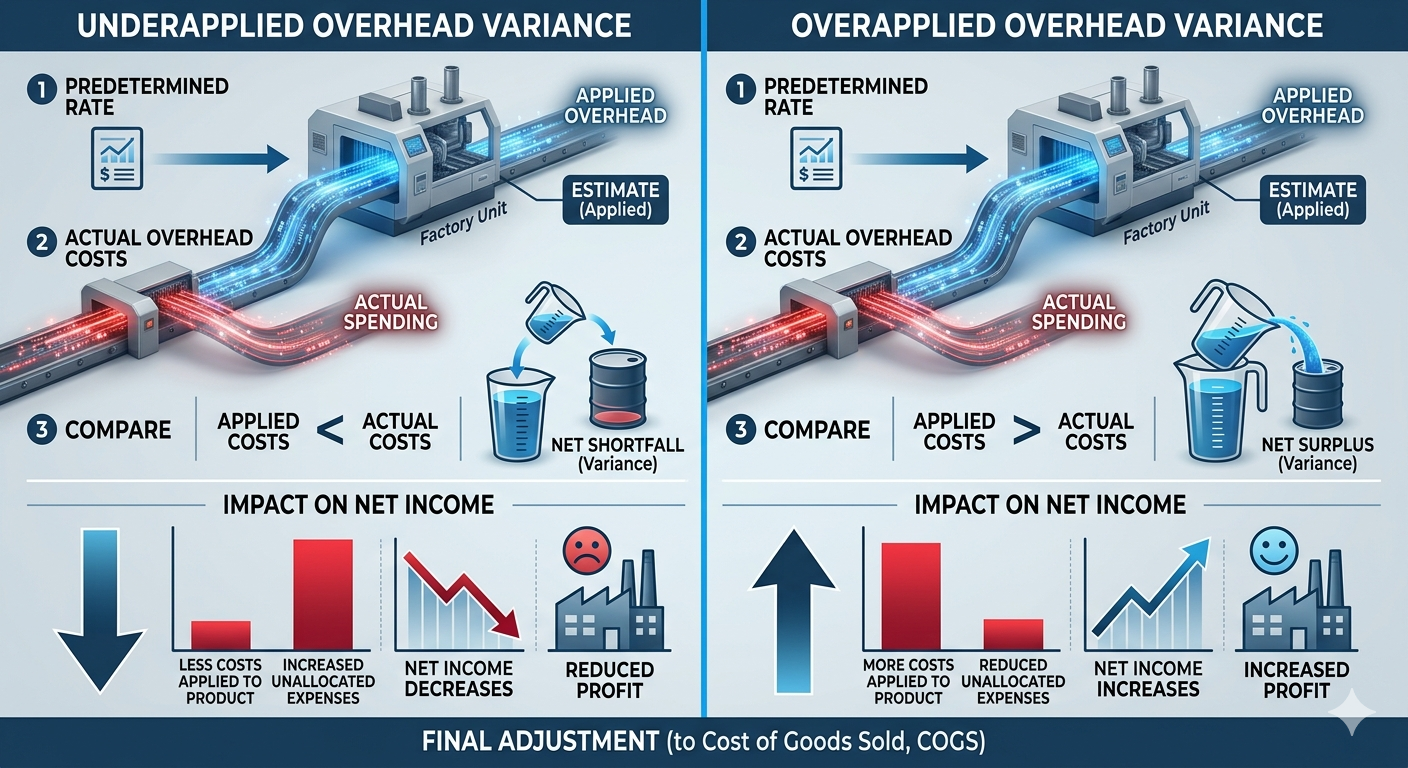

1) Underapplied vs. Overapplied

- Underapplied Overhead:

- Status: Applied Amount < Actual Amount.

- Meaning: You put less cost on the product than you actually spent. Profits will look artificially high (Overstated) until you correct it by adding the missing expenses.

- Overapplied Overhead:

- Status: Applied Amount > Actual Amount.

- Meaning: You put more cost on the product than you actually spent. Profits will look lower than they really are until you reduce the excess costs to reveal the true profit.

2) The “Real” Reasons for the Variance

- Spending Variance (Price): The price of overhead items (electricity rates, rent, insurance) went up or down unexpectedly. For example, a sudden spike in energy prices causes Underapplied overhead.

- Volume Variance (Activity): The actual total activity (labor hours, machine hours) differed from the forecast. If the factory was busier than expected, you might end up with Overapplied overhead.

3) Case Study: The Effect of Adjusting Underapplied Overhead

- Before Adjustment: The ledger shows less expense than what was actually spent.

- Profit Status: Because expenses are low, the book profit is Overstated.

- Adjustment Process: Add the “missing” cost to the Cost of Goods Sold (COGS).

- After Adjustment: Expenses increase, and profit is normalized to a Lower (more accurate) level.

4. Year-End Adjustments: Reconciling Prediction with Reality

The final goal of accounting is to report actual costs. Therefore, at year-end, we must reconcile the “Applied” (estimated) figures with “Actual” expenditures.

1) Why Must We Adjust?

- Actual Cost Reporting: Financial statements for stakeholders must reflect reality. Leaving estimates on the books distorts the value of assets (Inventory) and expenses (COGS).

- Profitability Accuracy: Correcting variances helps managers judge exactly how much profit was made on specific product lines.

- Tax & Audit Compliance: Tax authorities require actual expenses. Leaving estimates could lead to legal or tax issues.

2) Why Not Carry the Variance Over to Next Year? (Non-deferral)

- Matching Principle: Costs incurred to generate revenue this year must be recorded this year. Carrying errors into next year distorts the profitability of both years.

- Asset Valuation: Ending inventory in the warehouse must reflect actual costs. Deferring the variance means the Balance Sheet will show inaccurate asset values.

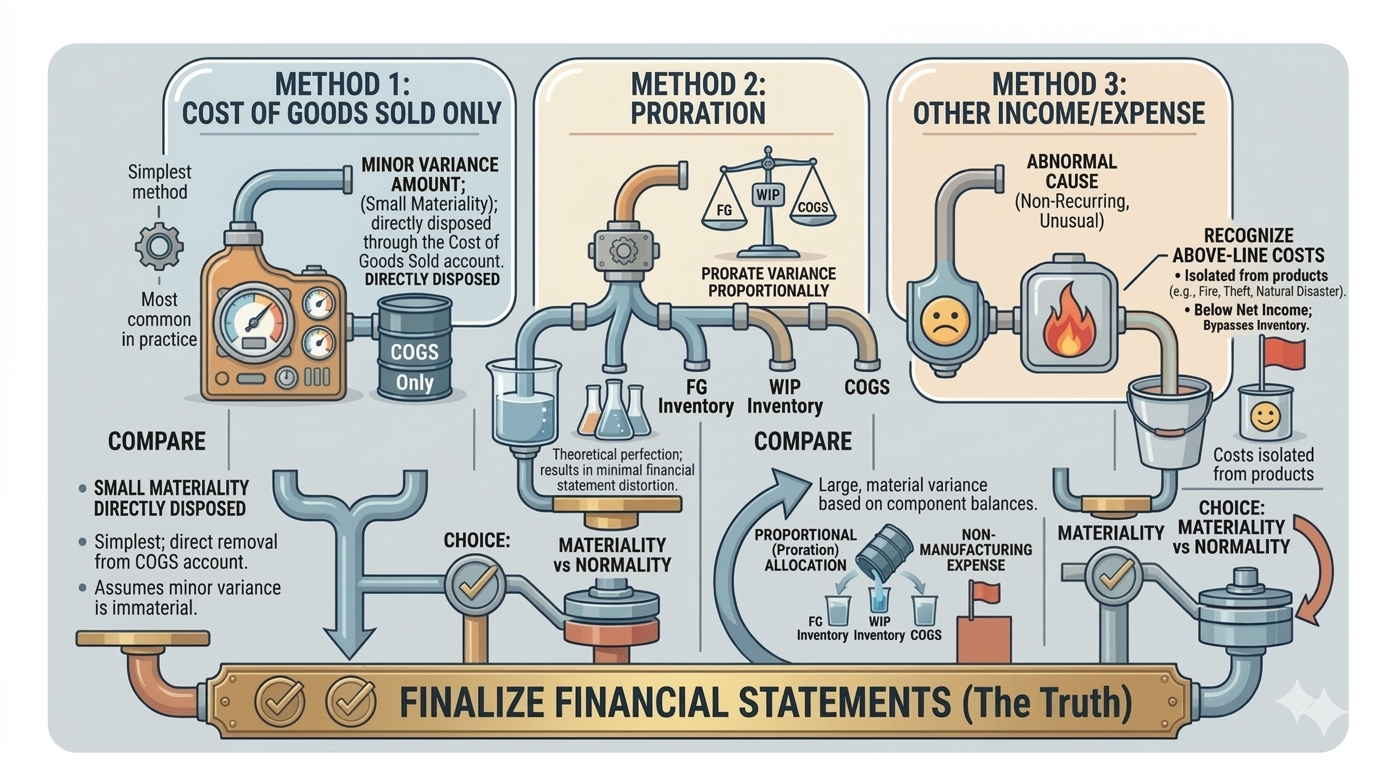

3) The Three Methods of Adjustment

- Cost of Goods Sold (COGS) Method: The entire variance is closed into COGS. This is the simplest and most common method used when the variance is “immaterial” (small).

- Proration Method: The variance is split among Work-in-Process, Finished Goods, and COGS based on their relative balances. This is the most theoretically perfect method and is used when the variance is significant.

- Prorate : To distribute an amount proportionally among different accounts.

- Other Income/Expense Method: The variance is treated as a non-operating item. This is used when the gap was caused by an abnormal event like a fire or natural disaster, rather than standard production issues.

Conclusion: Key Takeaways

- The “Apply” Logic: Think of overhead as a coating on your product. Underapplied means the coating is too thin; Overapplied means it’s too thick.

- Timeliness vs. Accuracy: Normal Costing chooses speed (Timeliness) during the year and reconciles for accuracy at the end of the year.

- Strategic Compass: A large variance is a signal that your “budgeting” or “operational efficiency” needs a course correction for the next fiscal cycle.

AI Disclosure: Created in collaboration with Google Gemini. All core content was authored, reviewed, and edited by the author.