In 20th-century traditional accounting, “spending money” was merely a historical footprint—a cold record of what had already left the bank. However, in 2026, behind the financial powerhouses like NVIDIA, a much more sophisticated strategy is at play. The way these tech giants handle Cost versus Expense is not just bookkeeping; it is a high-stakes survival strategy.

To truly grasp the value of modern business, we must look beyond the simple act of “spending.” We must understand the “magical transformation” where an expenditure evolves into future revenue. What determines whether a dollar spent becomes a valuable seed or a mere wisp of smoke?

1. Evolution: When Numbers Become a Strategic Weapon

In the past, cost management was the domain of “frugality”—the image of a factory foreman counting pennies and nagging workers to save on raw materials. It was about “saving.”

Today, however, Cost has transformed into a high-level indicator of a company’s R&D prowess and manufacturing efficiency. As the global AI semiconductor war reaches a fever pitch, cost management has moved beyond “keeping the books” into the era of Strategic Cost Management (SCM). In this era, costs are not just tracked; they are engineered to design the company’s future value. Let’s dive into what makes this concept so vital.

2. Understanding Through Everyday Analogies

1) Cost = “The Invested Seed for Future Harvest”

In accounting, a “Cost” represents value that is being “stored” within the company before a product is sold.

- The Analogy: Imagine a specialty bakery owner who buys premium flour and organic sugar to bake artisan sourdough.

- The Characteristic: You don’t need to lament the money leaving your account just yet. These “seeds” are Assets. They sit in your warehouse (Balance Sheet) because they are destined to transform into a “finished loaf”—a product with significantly higher value.

- The Real-World Scenario: When Tesla invests in lithium for EV batteries or pays labor to assemble a Model Y, that money is protected under the label “Cost” (specifically, Inventory) until the car is finally delivered to a customer.

2) Expense = “The Energy Consumed to Drive Revenue”

An “Expense” is value that has been “used up” or has expired in the immediate process of earning revenue.

- The Analogy: This is the monthly rent for the bakery storefront or the digital ad spend on Instagram to lure customers in.

- The Characteristic: This value vanishes the moment it is consumed. But don’t be mistaken—this “loss” is necessary to generate Revenue. The moment a customer buys that loaf of bread, the flour (Cost) you were saving also finally makes its move: it transforms into an “Expense” known as COGS (Cost of Goods Sold).

- The Real-World Scenario: When OpenAI pays its massive electricity bills for the servers running ChatGPT, that is an “Expense” consumed immediately to provide the service today.

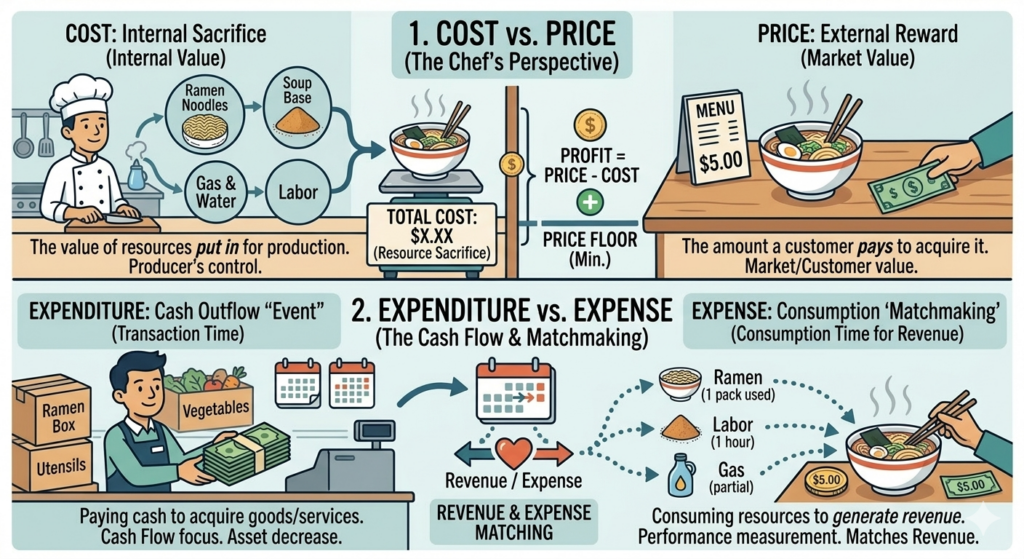

3. Academic Definitions: Cost vs. Price

Beyond simple analogies, we must define “Cost” with academic rigor and clarify why it is fundamentally different from “Price,” a term often confused by the general public.

What is “Cost” in the Professional Sense?

- Sacrifice of Resources: Cost is the monetary measure of resources consumed or sacrificed to achieve a specific objective, such as manufacturing a chip or developing software. (Costs are consumptions or sacrifice of resources.)

- Goal Orientation: It is not a random loss of money; it is the specific amount you must give up or pay to secure something of value. (Amount that you must give up or pay to get something.)

- Future Potential: Cost is an investment for “future revenue.” It is strictly distinguished from “Loss,” which is money that disappears without any corresponding benefit.

Cost vs. Price

- Cost: The actual expenditure made by the Producer to secure goods or services. (Amount of expenditure made in order to secure some goods or services.)

- Price: The amount a Customer is willing to pay to acquire that product or service. (Amount a customer is willing to pay for a product or service.)

The Key Distinctions:

- Perspective: Cost is an “Internal Sacrifice” controlled by the producer; Price is an “External Reward” determined by the market.

- Function: Cost acts as the “Floor” (the minimum boundary) for the price. The delta between the Price and the Cost is where the company’s profit lives.

- Example: If a chef spends $4 on organic flour, yeast, and labor for one pizza, that $4 is the Cost. The $22 listed on the menu is the Price.

4. Expenditure vs. Expense

Many people use these terms interchangeably, but in Strategic Cost Management, they represent two very different financial states.

- Expenditure (The Event): This is a “Cash Flow” event. It is the act of paying cash or taking on debt to acquire a resource. It tells us about the company’s Liquidity.

- Expense (The Expiration): This is a “Performance” event. It occurs when a resource is consumed to earn revenue. It tells us about the company’s Net Income.

The Logic of the Process:

Imagine a restaurant owner who goes to a wholesale club and buys a massive crate of pasta for $500.

- The moment the credit card is swiped, that is an Expenditure.

- The chef takes enough pasta for one serving; that specific portion is the Cost.

- Only when the customer eats the meal and pays the bill does that $5 portion transform into an Expense on the income statement.

Summary: Expenditure is about “When the money left,” while Expense is about “When the value was used to make a profit.”

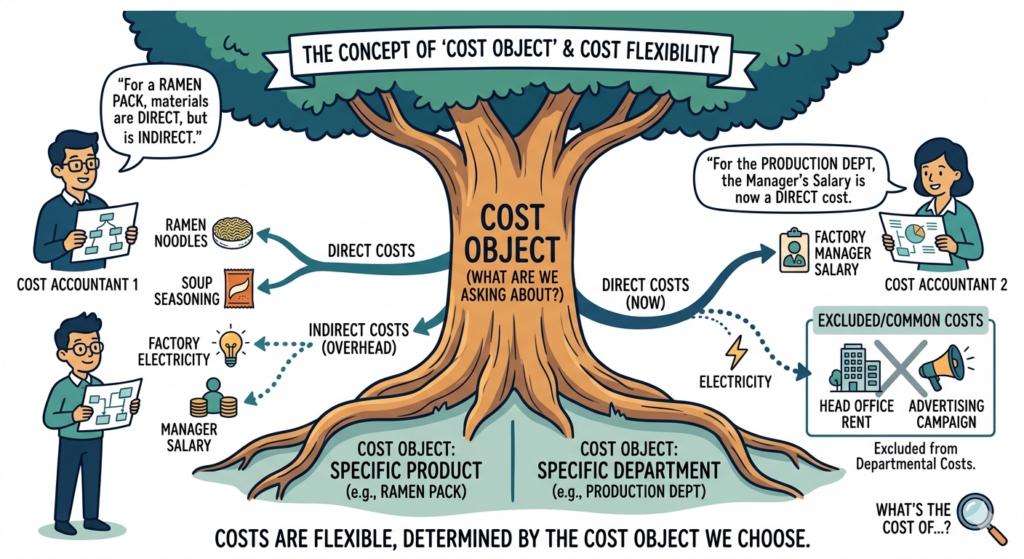

5. The “Cost Object”: The Secret to Flexible Accounting

Cost is not a fixed, absolute number. It is a “living” concept that changes based on the question: “What do we want to know the cost of?” In professional accounting, we call this the Cost Object.

1) Defining the Cost Object

A cost object is any activity, product, service, or organizational unit for which a company wants a separate measurement of costs. (Anything for which a company wants to measure costs.)

2) The Fluidity of Costing

The same dollar spent can change its “personality” depending on the cost object. This is why we say: “Costs differ depending on the cost object.”

3) Practical Case Study: General Mills (Cereal Production)

Consider a global food company like General Mills producing Cheerios.

- Case A: The Object is “One Box of Cheerios”The cardboard for the box and the oats inside are Direct Costs—they belong only to that box. However, the factory’s electricity and the plant manager’s salary are Indirect Costs. They support millions of boxes, so we must “allocate” them using a formula.

- Case B: The Object is “The Production Department”Now, that plant manager’s salary—which was an indirect cost for a single box—becomes a Direct Cost for the department. Why? Because the manager is a direct expense of running that specific organizational unit.

Conclusion: Cost is not a static value; it is a strategic variable that shifts based on “what” you are trying to analyze.

6. Strategic Cost Management: Shifting from Assets to Profits

We have moved past the era of keeping a “factory checkbook.” We are now in the era of Resource Intelligence.

- The Manufacturing Blueprint: Understanding how raw materials, labor, and overhead condense into a single asset called “Inventory.”

- Controlling Period Costs: Managing rent, administrative salaries, and marketing—costs that vanish with time regardless of how much you produce—to increase the company’s financial “stamina.”

- The Matching Principle: By recognizing costs as expenses only when the revenue is realized, we can accurately measure the true health and profitability of the business.

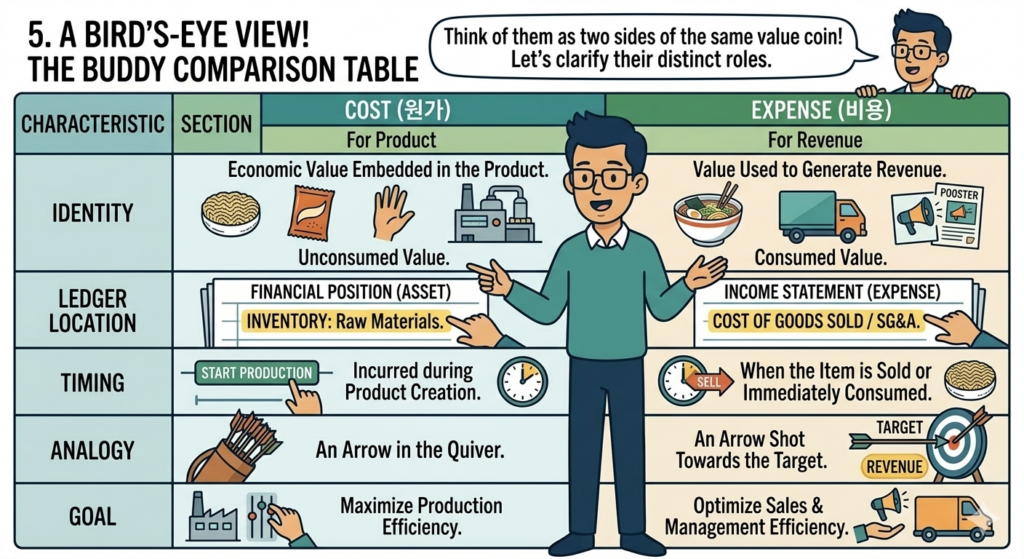

7. At a Glance: The Strategic Comparison Table

| Feature | Cost (Cost) | Expense (Expense) |

| Identity | Economic value “stored” in a product/asset | Value “consumed” to drive revenue |

| Ledger Position | Balance Sheet (Asset) | Income Statement (Expense) |

| Timing | Incurred during creation/production | Recognized at the time of sale/consumption |

| Analogy | A sharpened “Arrow” sitting in the quiver | An “Arrow” shot into the target |

| Strategic Goal | Production efficiency & Value creation | Sales & Management optimization |

Conclusion: Key Takeaways

- Cost is a Bridge: It is the bridge between spending money and making a profit. Until that bridge is crossed (a sale), the cost remains a valuable Asset.

- Context is King: There is no such thing as a “fixed cost” without a Cost Object. Always ask: “What are we measuring?”

- Strategic Mindset: Successful businesses like NVIDIA don’t just cut costs; they strategically allocate them to ensure that every “sacrifice of resources” today yields a massive “return on investment” tomorrow.

AI Disclosure: Created in collaboration with Google Gemini. All core content was authored, reviewed, and edited by the author.