In an era where AI and automation have redefined corporate efficiency, the true challenge for leadership is no longer managing what is visible, but mastering the “invisible” overhead that quietly erodes profitability. Traditional accounting often fails to capture the intricate dance between complex technology and human labor. To navigate this, executives must shift their perspective: costs do not simply happen—they are consumed by specific activities. This guide provides a strategic roadmap for deconstructing the architecture of Activity-Based Costing (ABC) and its implementation in the high-stakes environment of modern healthcare.

1. Designing and Controlling the Invisible Flow of Costs

In the modern corporate landscape, cost structures are no longer straightforward. As AI and automation systems are integrated, direct labor costs have plummeted, while a massive, “invisible” mountain of indirect overhead now dictates a company’s profitability. To make precise decisions in this complexity, executives must move beyond seeing costs as something that simply “occurs.” Instead, they must understand the technical reality: costs are consumed through specific activities. Today, we will dissect the infrastructure of Activity-Based Costing (ABC) and the rigorous process of its implementation.

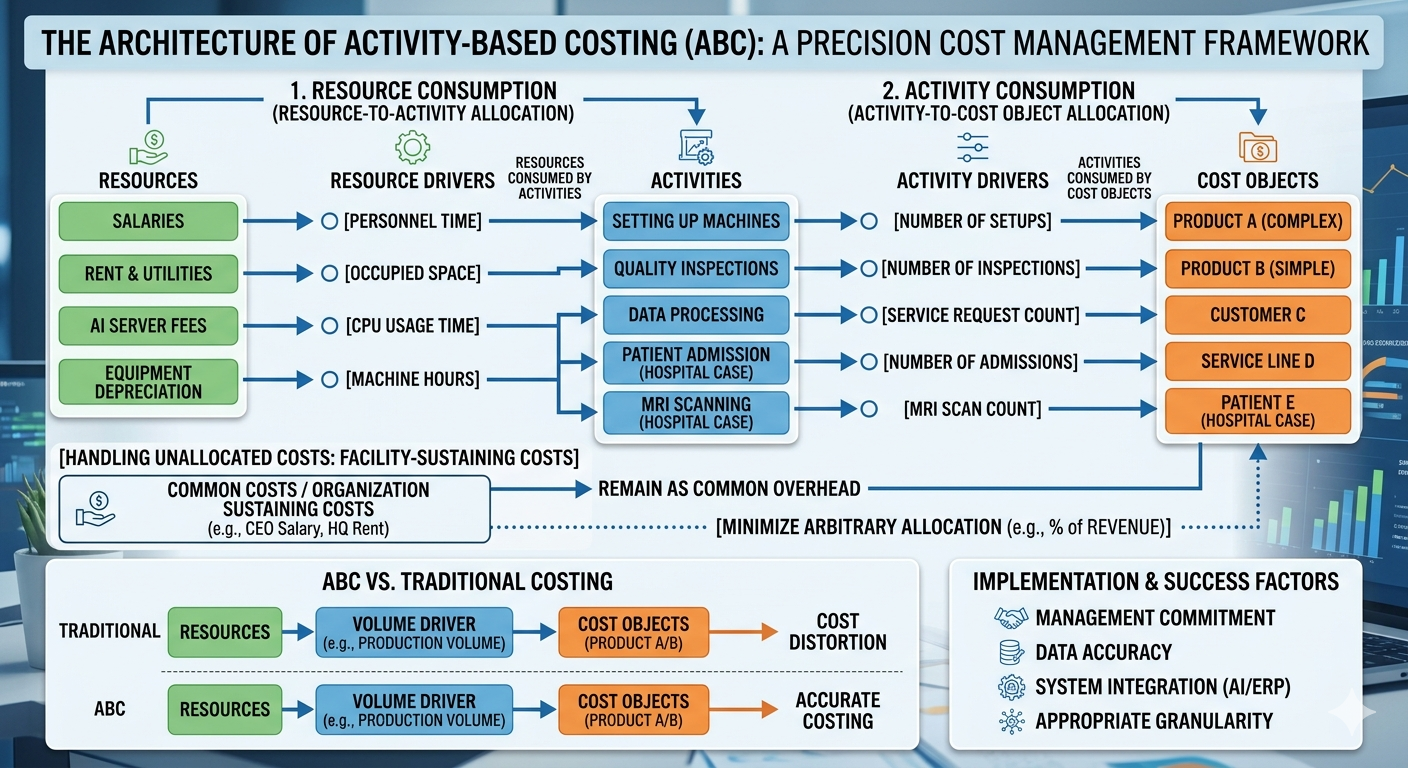

2. The Four Pillars of the ABC Framework

To design a functional ABC system, one must first define four fundamental concepts:

- Resources: These are the economic sources a company spends money on to perform activities. Examples include salaries, rent, utilities, and AI server fees.

- Activities: These are specific units of work that consume resources to create value. Common activities include setting up machines, quality inspections, data labeling, and patient consultations.

- Cost Objects: The final targets where costs are aggregated. This includes not only end products but also specific customers, service lines, or individual patient cases.

- Drivers: The bridges that connect resources, activities, and cost objects through a cause-and-effect relationship.

- Resource Drivers: The criteria for allocating resource costs to activities (e.g., allocating rent based on square footage or server fees based on CPU usage time).

- Activity Drivers: The criteria for allocating activity costs to the final cost objects (e.g., number of inspections, number of setups, or service request counts).

3. The Technical Process: Two-Stage Allocation

ABC follows a two-stage allocation process, using “activities” as a vital midway station rather than dumping resource costs directly onto products.

- Stage 1 (Resources → Activities): The total resource costs incurred are distributed into various activity pools based on consumption. For instance, the salary of an administrative department is allocated to “purchasing” and “accounting” activities based on the percentage of time spent on each.

- Stage 2 (Activities → Cost Objects): The aggregated activity costs are then assigned to the products or services that triggered those activities. If a specific product line required ten quality inspections, the cost of those inspections is attributed directly to that product.

- Handling Unallocated Costs: Not all costs have a clear causal link to an activity. “Facility-Sustaining Costs,” such as the CEO’s salary or headquarters rent, are difficult to match with specific product activities. While some firms arbitrarily allocate these based on revenue, the core principle of ABC is to minimize such arbitrary moves to maintain the purity and accuracy of the data.

4. ABC vs. Traditional Costing: The Reality of Distortion

Traditional costing relies heavily on production volume (unit-level drivers). This often leads to Cost Distortion, where low-volume but highly complex products are significantly undercosted. When switching to ABC, it is common to see the calculated cost of complex products rise by 20% to 50%, while the cost of simple, mass-produced items falls.

However, ABC is not a silver bullet. Its primary drawback is that it is expensive to design and maintain. The process of defining hundreds of activities and collecting data can sometimes cost more than the value of the information gained. Furthermore, if activity definitions are too subjective, the objectivity of the data can be compromised.

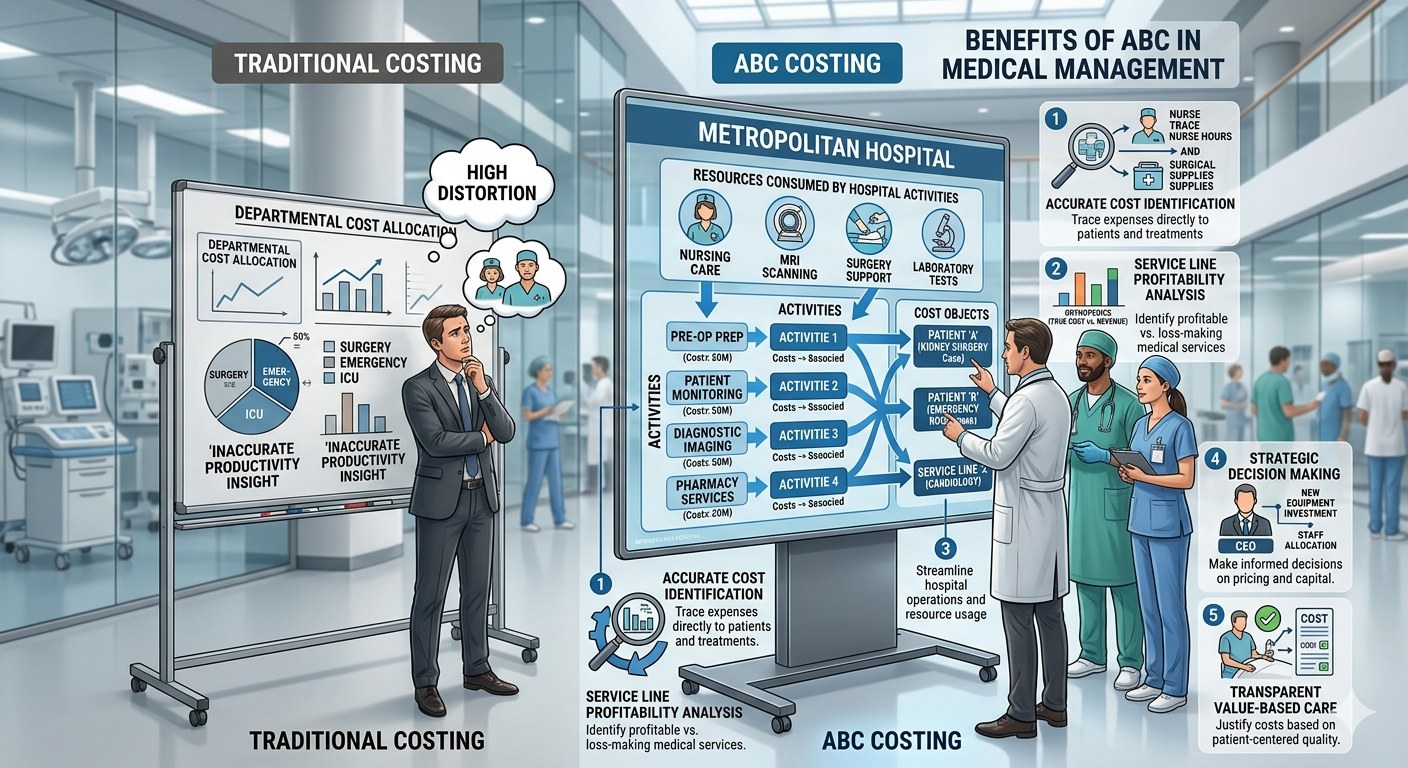

5. Precise Analysis: Implementing ABC in Healthcare Management

“How much does it truly cost to treat a single patient?” In a hospital setting, the proportion of indirect costs—such as medical equipment maintenance, nursing labor, and administrative overhead—is overwhelmingly high. Traditional methods that simply look at revenue by department cannot tell you if a specific surgery is truly profitable or running at a loss.

The Components of Hospital ABC

- Resources: Salaries for doctors and nurses, operating room rent, MRI/CT depreciation, and medical supplies.

- Activities: Patient registration, blood collection, MRI scanning, surgical prep, and inpatient nursing care.

- Cost Objects: A specific patient, a Diagnostic Related Group (e.g., appendectomy cases), or a specific department (e.g., Surgery).

The Logic of Drivers in Medicine

- Resource Drivers: Allocating operating room rent to “Surgical Activities” based on [Room Occupancy Time] or allocating nurse salaries to “Medication Activities” based on [Time Spent per Task].

- Activity Drivers: Allocating “MRI Scanning Activity” costs to a patient based on the [Number of Scans] or “Registration Costs” based on the [Count of Admissions].

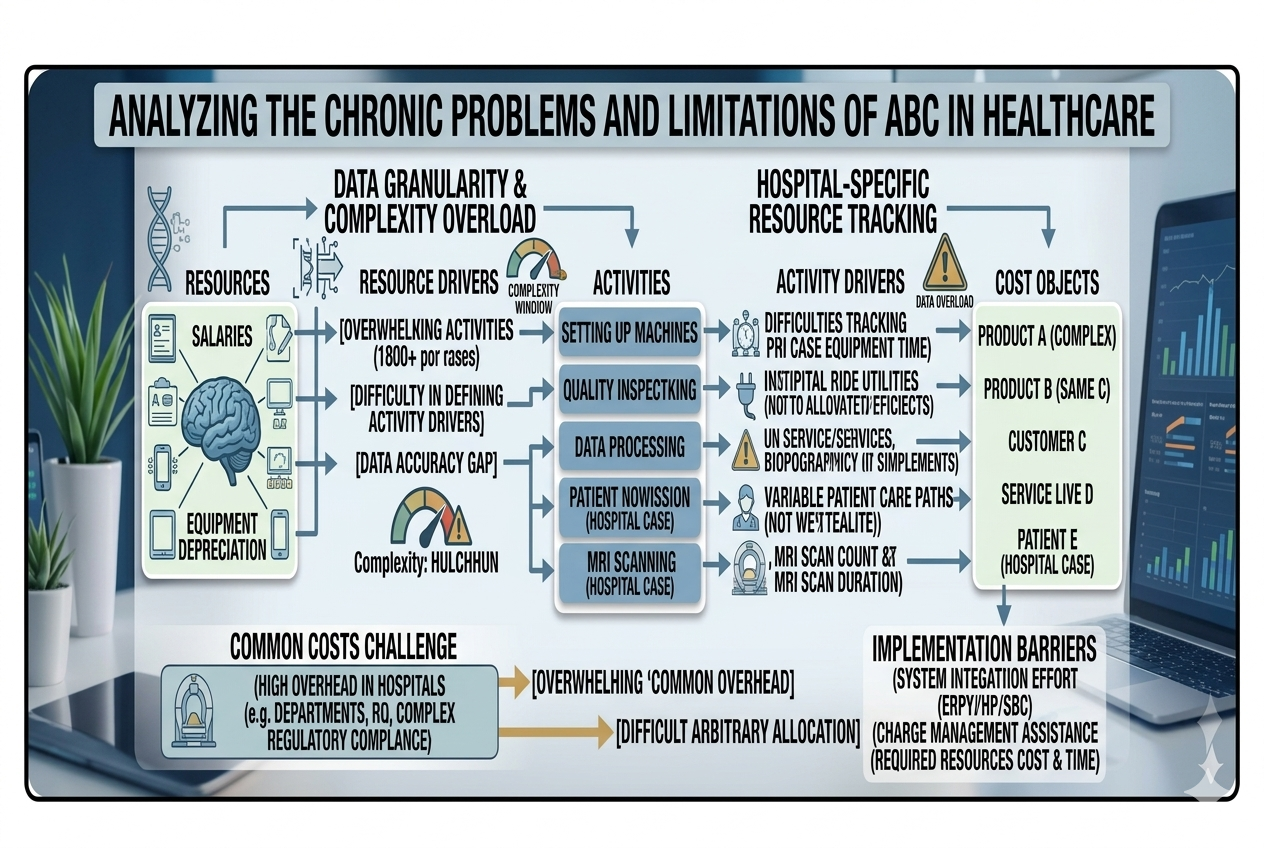

6. Chronic Problems and Limitations of ABC in Healthcare

Despite its precision, ABC in hospitals often hits a wall due to the non-standardized nature of medical work and the intrinsic value of human life.

Measurement Complexity and Subjectivity

Unlike a factory machine that runs at a constant speed, the resources required for a patient vary wildly based on their condition.

- Ambiguity in Activity Definition: An “Initial Consultation” for a patient with a minor cold versus a patient with a complex chronic illness requires vastly different mental energy and time. Grouping them as one “standard activity” distorts costs, but over-segmenting them causes administrative costs to explode.

- Data Collection Hurdles: It is practically impossible for medical staff to log every minute spent with every patient. Relying on periodic surveys or estimates leads to the “Data Accuracy Gap,” a chronic issue in healthcare ABC.

The Challenge of Common Costs

Hospitals have dozens of support departments (IT, HR, Facilities, Sterilization) that provide services to each other in a complex web.

- High Overhead: The “Facility-Sustaining” portion of a hospital is massive. When these costs are allocated using arbitrary metrics like “Number of Beds,” the precision of ABC is diluted.

- System Integration Effort: Reflecting mutual support between departments (Reciprocal Allocation) requires sophisticated ERP systems and specialized personnel. Often, the cost of maintaining this system exceeds the financial benefit of the data.

Quality vs. Cost: The Ethical Trap

ABC is a tool for efficiency, but it risks overlooking the “Quality of Care.”

- The Trap of Non-Value-Added Activities: From a pure ABC perspective, double-checking a patient’s identity or spending extra time comforting a family might look like “inefficiency” to be eliminated. However, these are essential for patient safety and satisfaction.

- Capacity and Idle Assets: ERs and ICUs must maintain staff and equipment even when there are no patients. ABC might label this as “Idle Capacity” (inefficiency), but in public health, this is a “Ready Asset” essential for emergencies.

Conclusion: Key Takeaways

- From Volume to Activity: Move away from volume-based allocation. Understand that complexity, not just quantity, drives costs.

- Data over Intuition: Use Resource and Activity Drivers to map the invisible flow of money, especially in high-overhead environments like hospitals.

- The Balanced View: While ABC provides precision, it must be balanced with the qualitative value of medical care. Efficiency should never come at the cost of patient safety.

- Strategic Success: Successful ABC requires strong executive commitment, seamless AI/ERP integration, and finding the “Sweet Spot” in granularity—neither too simple nor too complex.

AI Disclosure: Created in collaboration with Google Gemini. All core content was authored, reviewed, and edited by the author.