n the past, investing was simply about becoming an owner of a highly profitable company. Today, however, investing has evolved into a strategic battle of asset protection—it is not just about how much money you make, but how much of it you actually keep.

While mutual funds and exchange-traded funds (ETFs) are excellent vehicles for growing your wealth, they come with entirely different tax obligations. In 2026, smart investors must look beyond gross returns and focus on real, net-of-tax returns. Investing without understanding taxes is like ordering a meal based solely on the menu price, completely ignoring the delivery fees and sales tax that show up on the final bill.

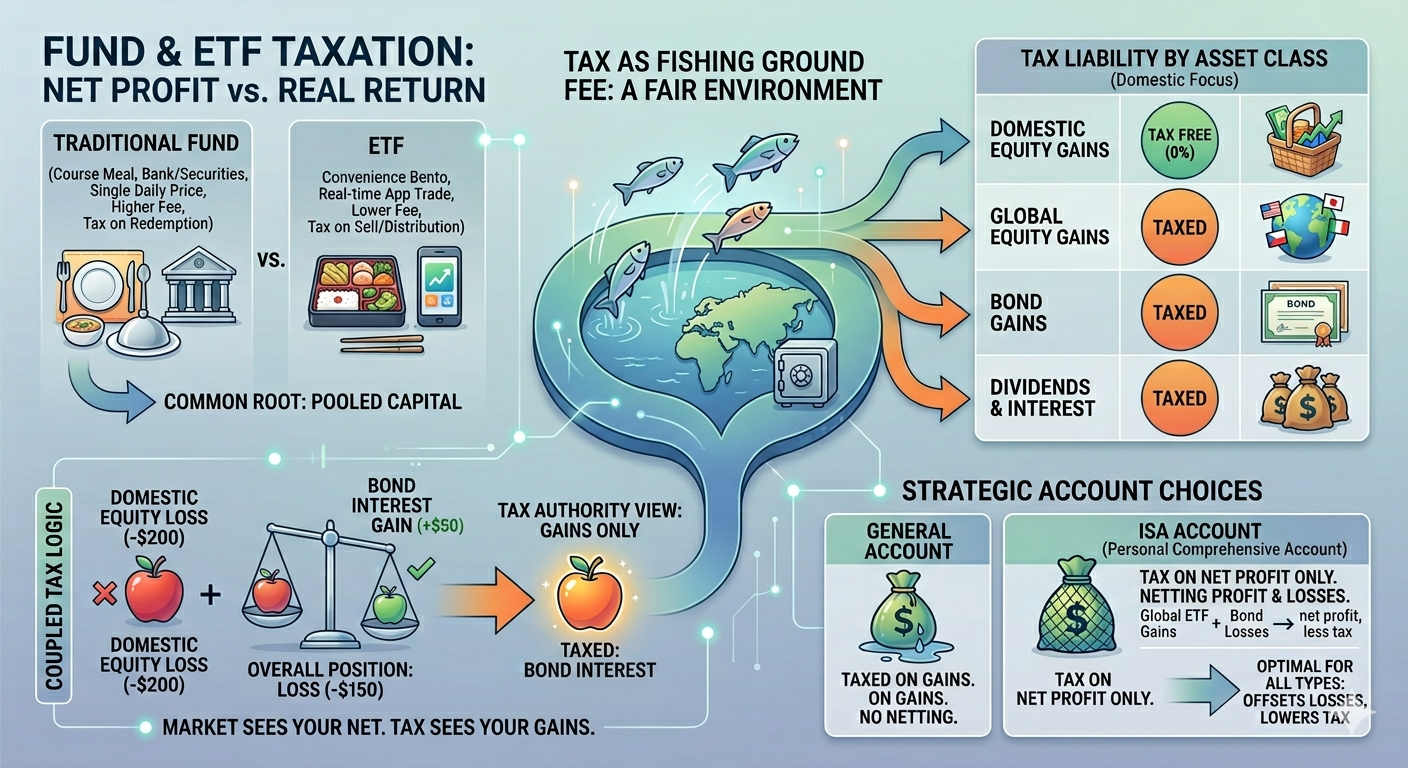

1. Breaking Down the Terms with Everyday Analogies

To understand the core differences between mutual funds and ETFs—and how the IRS or CRA views them—let’s break down the definitions and look at how they operate in the real world.

Decoding ‘Mutual Fund’ vs. ‘ETF’

- Mutual Fund: A pool of capital collected from many investors to invest in securities like stocks or bonds. Think of a traditional mutual fund as a multi-course catered dinner. It is managed by a professional chef (the portfolio manager), and you receive it at a set time (the end of the trading day) for a fixed price.

- Exchange-Traded Fund (ETF): A fund that holds a basket of assets but trades on a public stock exchange, just like individual shares. Think of an ETF as a premium grab-and-go meal kiosk. It holds the same high-quality ingredients as the catered dinner, but it is broken down into individual portions that you can buy or sell at any exact moment throughout the trading day.

Taxes as the ‘Fishing Hole Maintenance Fee’

Why do we pay taxes on our investment returns? Think of the financial market as a well-regulated fishing hole. The reason you can safely catch fish (generate returns) is that the government maintains the docks, stocks the lake, and enforces the rules to keep the environment secure. Your investment taxes are essentially the infrastructure and maintenance fees required to keep the fishing hole thriving.

2. Tax Variations Based on Underlying Assets

The tax “toll” you pay depends entirely on what types of assets you hold inside your investment basket.

| Asset Class / Return Type | Scenario | General Tax Treatment (Non-Registered Accounts) | Real-World Analogy |

|---|---|---|---|

| Domestic Capital Gains | Selling domestic stocks at a profit. | Subject to capital gains tax (typically only a portion of the gain is taxable). | Selling a rare collectible online for a clean profit. |

| Foreign Capital Gains | Profiting from international or global stocks. | Fully taxable capital gains, often subject to foreign withholding taxes. | Paying customs duty when importing luxury goods. |

| Fixed-Income Capital Gains | Profiting from selling corporate or government bonds. | Taxed as capital gains or interest income depending on the structure. | Selling a debt note to someone else at a premium. |

| Dividends and Interest | Holding assets that pay regular cash distributions. | Dividends may receive tax credits (domestic), while interest is taxed at your full marginal rate. | Receiving a predictable monthly allowance or rental check. |

3. The Unforgiving Logic of the Tax Code: Paying Taxes on a Net Loss

One of the most frustrating scenarios for retail investors is seeing their overall portfolio shrink, yet still receiving a tax bill at the end of the year. You might ask, “If my total principal went down, why am I being taxed?”

This happens because tax authorities do not look at your portfolio’s holistic performance sheet; instead, they evaluate each transaction as an isolated event.

Imagine you lose $2,000 on a domestic stock sale (which results in a capital loss), but you earn $500 in bond interest during the same year. Geometrically, your pocket is down $1,500. However, if those asset classes cannot be legally offset, the tax code dictates: “We cannot subsidize certain non-deductible losses, but we will absolutely tax you on the $500 interest income you pulled in.”

Market Catchphrase: The market looks at the total weight of your jacket, but the tax collector only cares about the single ripe red apple hidden inside your pocket.

4. Mutual Funds and ETFs: Siblings with Different Structures

Though ETFs are structurally a modern evolution of mutual funds, their differing mechanics alter how they are taxed and managed.

| Category | Traditional Mutual Fund | Exchange-Traded Fund (ETF) |

|---|---|---|

| Trading Mechanism | Bought/sold through banks or brokers; priced once per day at market close. | Traded in real-time on stock exchanges via trading apps. |

| Management Fees (MER) | Generally higher due to active management and administrative overhead. | Generally lower due to passive tracking of automated indexes. |

| Tax Settlement | Capital gains are often passed through to remaining shareholders annually. | Highly tax-efficient; capital gains are primarily triggered only when you sell your shares. |

Sheets로 내보내기

5. Essential Rules of ETF Taxation

The internal makeup of an ETF dictates your tax liability:

- Broad-Market Equity ETFs: ETFs tracking major domestic indexes are highly tax-efficient. Thanks to the “in-kind” creation and redemption process of ETFs, portfolio managers can rebalance the fund without triggering capital gains distributions for the shareholders.

- Specialty ETFs (Foreign, Bond, Commodities): Investing in international, fixed-income, or derivative-heavy ETFs will expose you to regular income tax rates on distributions, alongside potential foreign withholding taxes on dividends.

- Distributions (Dividends & Interest): Any cash distributions paid out by an ETF while you hold it are taxable in the year they are received, regardless of whether the fund’s underlying price went up or down.

6. Winning Tax Strategies for Every Investor Profile

① The Aggressive Growth Investor (Young Professionals)

- The Situation: You have a long time horizon, lower initial capital, and a heavy interest in volatile international or tech ETFs.

- The Strategy: Because foreign equities carry higher tax complexities, maximize your tax-advantaged accounts first (such as a Roth IRA in the US or a TFSA in Canada). These accounts allow your capital gains to compound and be withdrawn entirely tax-free, protecting your highest-growth assets.

② The Tax-Averse High Earner

- The Situation: You are in a high income bracket and face heavy hits from progressive tax rates and investment income surcharges.

- The Strategy: Shift focus toward broad-market index ETFs rather than actively managed mutual funds to avoid annual capital gains distributions. Additionally, aggressively utilize employer-sponsored plans (like a 401k or RRSP) to defer your tax liabilities until retirement, when you will likely sit in a lower tax bracket.

③ The Income-Focused Investor (Retirees)

- The Situation: Protecting your principal is paramount, and you require reliable monthly distributions to cover living expenses.

- The Strategy: Focus on high-quality dividend or covered-call ETFs that offer stable payouts. To optimize this, keep interest-bearing bond ETFs inside sheltered tax accounts, while holding tax-credited domestic dividend ETFs in non-registered accounts to capitalize on lower preferential tax rates.

Conclusion: Key Takeaways

Navigating the financial landscape in 2026 requires looking past surface-level yields.

- Prioritize Tax Efficiency: Remember that ETFs generally hold a structural tax advantage over mutual funds by preventing internal capital gains distributions from hitting your tax return.

- Location Matters: It is not just about what you buy, but where you hold it. Align your high-tax assets with tax-sheltered accounts to shield your returns.

- Focus on Net Wealth: Always evaluate your investment performance based on what lands in your bank account after fees and taxes. By choosing the right vehicle and account type, you ensure that your hard-earned money stays exactly where it belongs: working for you.

AI Disclosure: Created in collaboration with Google Gemini. All core financial insights and content were originally authored, reviewed, and curated by the author for precision and North American market relevance.