If you have ever run a corporate finance department or managed the treasury of a growing organization, you have likely asked yourself this question: “I am already buried under balance sheets and income statements. Do I really need to spend valuable time and resources building a complex cash flow statement every month? Isn’t this just a decorative report for external auditors?”

It is true that constructing a cash flow statement is a labor-intensive, costly process. Accountants must dissect every single ledger account and translate accrual-based data into actual cash inflows and outflows. However, when you look at it through a cost-benefit lens, the verdict is clear: the benefits of maintaining a rigorous cash flow statement vastly outweigh the operational costs. It is the ultimate diagnostic dashboard for any business leader.

Let us break down why this statement is indispensable across four critical areas of financial management.

1. Verifying Quality of Earnings: Detection vs. Creative Accounting

| Cost | Benefit |

| The time and payroll expenses required for financial staff to reverse-engineer micro-level accounts—such as accounts receivable and inventory—into a cash-basis format. | A powerful risk-hedging tool that instantly exposes artificial profit inflation, such as channel stuffing (forcing excess inventory onto distributors) or fake inventory accumulation. |

Practical Application: “Exposing the Illusion of Net Income”

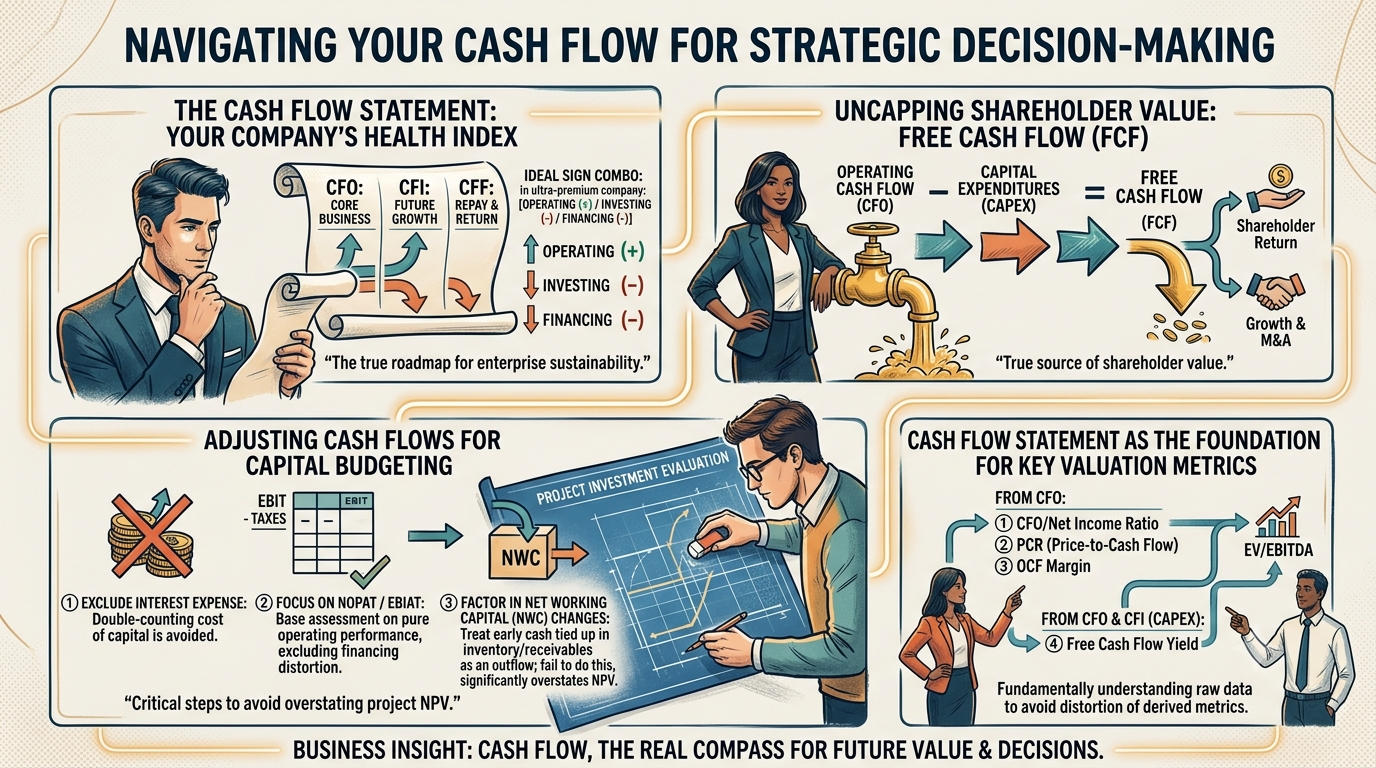

Under modern accrual accounting, net income can be highly elastic. Legally and within standard accounting frameworks, management can adjust the timing of revenue recognition. For example, if a company signs a major contract, it can record the revenue immediately, causing net income to skyrocket even if not a single dollar has cleared the bank.

This is where the Operating Cash Flow (OCF) section of the cash flow statement acts as a truth serum. It only records the actual cash that hits your corporate bank accounts. If a company reports $5 million in net income but shows a negative $2 million in OCF, the finance team must immediately sound the alarm. The message to the CEO is simple: “On paper, we are thriving; in reality, our bloodline is choking because our capital is trapped in unpaid invoices and unsellable inventory.” The cost of compiling this data is negligible compared to the catastrophic opportunity cost of letting a business run blind on phantom profits.

2. Preventing “Profitable Bankruptcy”: Continuous Monitoring vs. Insolvency Protection

| Cost | Benefit |

| Internal resources dedicated to mapping monthly or quarterly cash schedules and meticulously tracking fluctuations in net working capital. | Absolute control over sudden cash mismatches, effectively eliminating the risk of going bankrupt while technically operating at a profit. |

Practical Application: “The Lifeline for High-Growth Ventures”

A surprising number of startups and expanding medium-sized enterprises go bankrupt precisely when their sales are hitting record highs. In the corporate world, this is often driven by a structural cash mismatch. A company must pay for raw materials, payroll, and rent on the first of the month, but its commercial clients might operate on 90-day or 180-day payment terms.

Implementing a rolling cash flow statement brings your working capital requirements into sharp focus. It shows exactly how much cash your inventory and receivables are consuming. Armed with this dashboard, a leader can make proactive, defensive decisions: “As our sales volume scales, our cash reserves are depleting faster. We need to secure a revolving line of credit or renegotiate our collection terms immediately.” Preventing sudden corporate death is a massive return on a minor administrative investment.

3. Capital Budgeting: Projection Costs vs. Capital Destruction Prevention

| Cost | Benefit |

| The strategic planning overhead required to simulate and forecast annualized cash inflows and outflows for future corporate projects. | The clarity to filter out financial illusions and select projects that yield genuine economic value using Net Present Value (NPV) and Internal Rate of Return (IRR). |

Practical Application: “The Strategic Compass for Future Investments”

Amateur leaders approve multimillion-dollar capital investments based solely on projected accounting profit margins. In capital budgeting, the cash flow statement serves as the ultimate forecasting tool.

When evaluating a new manufacturing plant or a product line, a sophisticated finance team completely ignores historical R&D or sunk costs—money that has already left the building and cannot be recovered. Instead, they isolate the incremental cash flows. They answer one question: “If we greenlight this project today, how much cash leaves our accounts right now, and exactly how much cash will return each month over the next five years?” By stripping away non-cash accounting adjustments like depreciation, this approach keeps the executive team grounded in the time value of money, preventing them from bleeding capital into vanity projects.

4. Structural Capital Optimization: Valuation Costs vs. Premium Financing Benefits

| Cost | Benefit |

| The sophisticated accounting overhead needed to consistently isolate Free Cash Flow (FCF) by subtracting capital expenditures from operating cash flow. | Elite-tier credit ratings, maximum leverage during venture capital rounds, seamless mergers and acquisitions, and clear metrics for shareholder distribution. |

Practical Application: “The Ultimate Metric of Financial Power: Free Cash Flow”

Global institutional investors and venture capitalists do not judge a company’s health by its net income; they look at Free Cash Flow (FCF).

FCF represents the cold, hard cash a business generates from its core operations after reinvesting the capital necessary to maintain its asset base. This is the unencumbered cash that a CEO can freely deploy to pay dividends, buy back shares, or acquire competitors. When your cash flow statement proves a track record of robust FCF, commercial banks lower your borrowing rates and investors assign a premium to your valuation. The financial returns from securing lower interest rates and attracting premium equity investments dwarf the operational cost of tracking FCF.

Conclusion: Key Takeaways

An income statement tells you what a business has promised to earn; a cash flow statement tells you what the business has actually collected. Managing an organization without a cash flow statement is the equivalent of driving a vehicle at top speed while looking exclusively at the speedometer (revenue) while ignoring the fuel gauge (cash). You have no idea when the engine will cut out.

For corporate leaders and senior finance executives, elevating the cash flow statement from a compliance obligation to a primary decision-making dashboard is non-negotiable. The administrative costs are minimal, but the benefit—the long-term survival and scalable growth of your enterprise—is absolute.

- Quality Matters: High net income is meaningless without positive operating cash flow. Always validate your profits against actual collections.

- Watch Working Capital: Revenue growth drains cash before it creates it. Monitor receivables and inventory to avoid growing yourself into bankruptcy.

- Focus on FCF: Optimize your business for Free Cash Flow to secure cheaper debt, command higher valuations, and maintain absolute operational freedom.

* This article was created in collaboration with Google Gemini AI. The author independently created, reviewed, and edited the content to ensure professional quality.