If past corporate financial management focused primarily on raw production costs and immediate sales metrics, modern strategic leadership relies heavily on an entirely different dimension: time.

As we navigate the highly complex and shifting macroeconomic landscape of 2026, corporate leaders and individual investors alike face a definitive choice. Will you act as a captain steering a ship lost in the fog—blind to how time subtly erodes the purchasing power of your capital, locking yourself into disastrous long-term contracts? Or will you build a highly precise financial compass based on present value and discount rates to maximize your enterprise assets? Whether you are a retail investor managing a personal portfolio or a chief financial officer at a multinational enterprise, the most critical capability you can possess is a crystal-clear lens through which to read the changing value of money over time.

1. Understanding the Time Value of Money Through Everyday Dilemmas

The concept of the time value of money is not an abstract academic theory; it is actively woven into our daily corporate banking systems, commercial loans, and executive pension negotiations.

The Immediate Choice vs. Delayed Return:

If someone were to offer you a straightforward choice: “Would you rather receive $100,000 cold cash today, or exactly $100,000 ten years from now?” every single person would choose the immediate payout. The rationale is entirely intuitive: if you take the money today and place it into a standard interest-bearing vehicle, it will compound over a decade into a significantly larger sum.

Conversely, when an executive evaluates an enterprise retirement package, asking: “Is it financially superior to collect a structured monthly annuity over the next twenty years, or should we demand a single, upfront lump-sum payout today?” they are actively engaging in the calibration of the Present Value of an Annuity.

Core Frameworks: Definitions and Analytical Systems

- Time Value of Money (TVM): This is the foundational financial principle stating that a dollar in hand today is inherently worth more than a dollar promised at a future date. This disparity exists because of inflation, the opportunity cost of interest, and the persistent presence of operational risk and uncertainty.

- Discount Rate: This is the specific mathematical rate used to convert a future sum of money into its present equivalent. It represents the penalty applied to future cash flows to account for the passing of time and risk—hence the term “discounting.” From an enterprise perspective, it functions as the minimum hurdle rate or the firm’s true cost of capital.

- Strategic Synchronization: Ultimately, this framework serves as an enterprise valuation metric. By aligning every erratic, multi-year cash flow back to a single, unified point in time, leadership can eliminate superficial distractions and compare competing investments on an apples-to-apples basis.

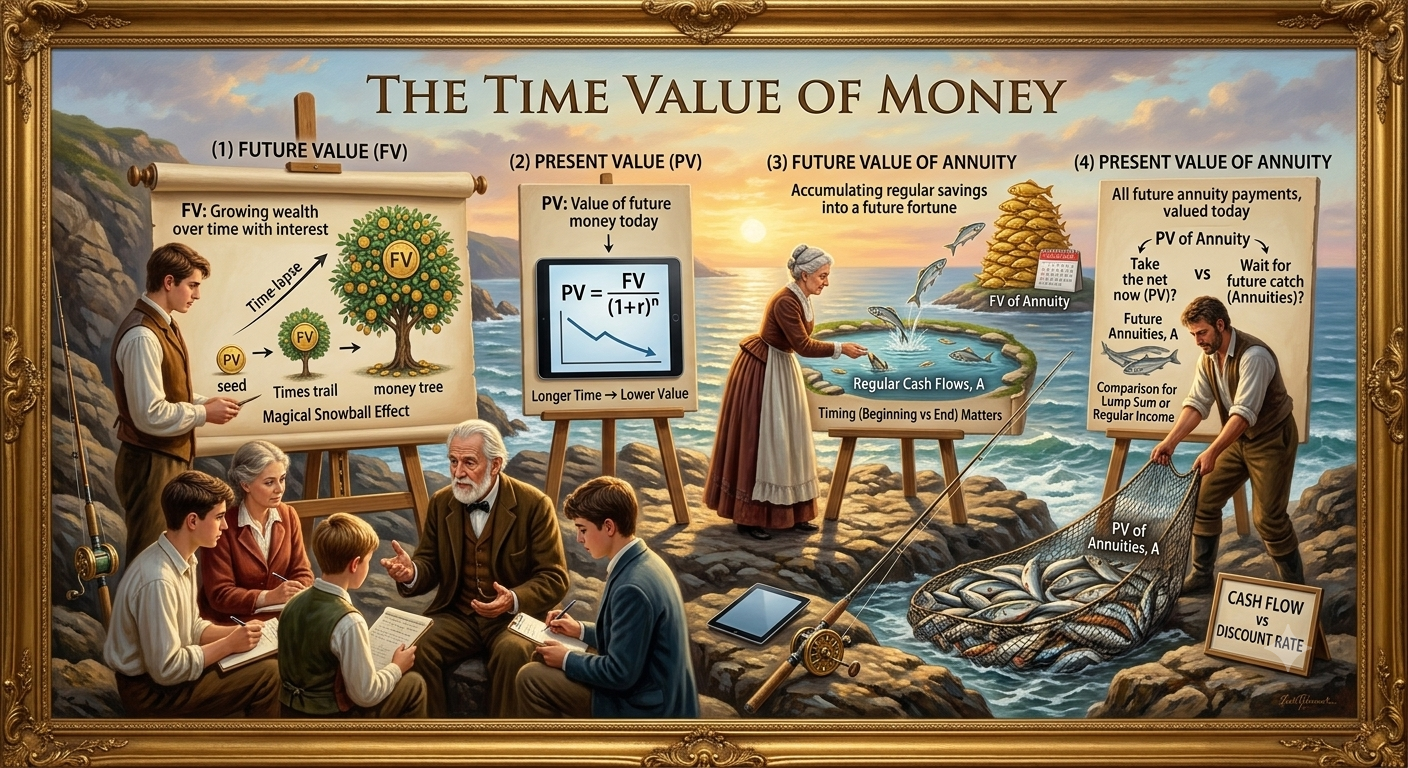

2. The Four Pillars of the Time Value of Money

To prevent formatting errors on mobile screens and various content management systems, we have bypassed dense, rigid equations in favor of highly intuitive, structural definitions.

1) Future Value (FV)

Future Value represents the total amount to which a specific sum of cash will grow over a defined time horizon when invested at a given compound interest rate.

- In Simple Terms: If an enterprise places $10 million into a multi-year corporate deposit yielding a 5% compound annual return, the Future Value is the exact terminal balance printed on the bank statement at the end of Year 3.

- The Core Mechanism: As time extends and interest rates climb, the future valuation swells exponentially through the compounding process.

2) Present Value (PV)

Present Value represents the current economic worth of a specific cash flow that is scheduled to be received or paid out in the future.

- In Simple Terms: If a firm holds a high-yield corporate bond maturing in five years with a face value of $10 million, calculating the Present Value answers one crucial question: “What is that future payout worth to my treasury right now?”

- The Core Mechanism: The further into the future a cash flow sits, and the higher the associated project risk (discount rate), the lower its current absolute valuation drops.

3) Future Value of an Annuity

This metric calculates the cumulative terminal value of a series of uniform, recurring cash contributions made at regular intervals over a specific period.

- In Simple Terms: If a company contributes $100,000 at the end of every month into a structured equipment replacement fund yielding 4% compounded annually, this represents the total aggregate cash available to purchase new machinery at the end of a 10-year horizon.

4) Present Value of an Annuity

This represents the total current worth of a stream of equal, recurring cash payments that will be received or paid out regularly over a future time frame.

- In Simple Terms: When deciding how to structure high-stakes commercial arrangements—such as evaluating long-term equipment leasing contracts or deciding whether a lottery winner should opt for a 20-year annual payout versus an immediate lump sum—this metric strips away non-cash illusions to expose the true financial winner.

Comparative Framework of Time-Value Methodologies

| Core Methodology | Direction of Capital | Common Enterprise Application | Critical Decision Variables |

|---|---|---|---|

| Future Value (FV) | Present → Future | Sinking fund accumulation, targeting terminal wealth reserves | Compounding frequency adjustments (Annual vs. Monthly compounding) |

| Present Value (PV) | Future → Present | Valuation of single-payment alternative investments, pricing corporate bonds | Establishing an accurate, risk-adjusted corporate discount rate |

| Future Value of an Annuity | Recurring → Future | Employee pension fund planning, structuring corporate cash reserves | Contribution timing mechanics (Annuity Due vs. Ordinary Annuity) |

| Present Value of an Annuity | Future Stream → Present | Heavy machinery lease-vs-buy evaluations, lottery payout optimization | Purchasing power degradation caused by systemic long-term inflation |

3. Forecasting Future Cash Flows and Structuring the Hurdle Rate

The operational integrity of any multi-year investment evaluation relies entirely on two pillars: the precision of your cash flow forecasting and the objective accuracy of your chosen discount rate.

The Standard for Future Cash Flow Projections

- Isolate Tangible Liquidity, Ignore Accounting Profits: Accrual-based net income routinely incorporates non-cash revenues like accounts receivable. When executing a time-value analysis, you must discard these accounting adjustments. Your financial models must strictly track real cash flowing into and out of your commercial bank accounts.

- Enforce the Principle of Conservatism: In corporate forecasting, future revenues are frequently delayed, while operational costs regularly exceed expectations. To insulate the corporate treasury against volatility, always apply a conservative discount to your inflows and a stress-test premium to your outflows.

The Criteria for Establishing the Discount Rate

The discount rate used to break down future cash flows is never an arbitrary guess. It is derived through structural corporate finance standards:

- Risk-Free Rate + Risk Premium: At a foundational level, the discount rate equals the yield on ultra-secure government sovereign debt (the risk-free rate) plus an additional percentage layer that accounts for the execution hazards of that specific project (the risk premium).

- The Corporate Standard (WACC): For most large-scale enterprise deployments, finance teams utilize the Weighted Average Cost of Capital. WACC represents the combined average cost a corporation incurs to secure capital from its debt holders and equity investors, serving as the baseline hurdle rate for all new initiatives.

4. Critical Management Pitfalls and Suboptimization Risks

When corporate executives deploy time-value frameworks in real-world scenarios without rigorous controls, they frequently fall into subtle traps that lead to massive capital suboptimization.

Pitfall 1: The Trap of the Static Discount Rate

- The Issue: Executing a high-stakes, 10-year infrastructure project and applying a uniform, identical discount rate across all ten years, ignoring the fact that the volatility of Year 1 is fundamentally lower than the uncertainty of Year 10.

- The Remedy: Because long-term risk intensifies over time, senior analysts must implement a risk-adjusted discount rate model, scaling the hurdle rate upward in later years to actively safeguard corporate assets against long-term operational failure.

Pitfall 2: Confusing Real Cash Flows with Nominal Discount Rates

- The Issue: Injecting raw, nominal dollar figures into a present value calculator without adjusting for inflation, even while systemic inflation is driving up structural costs annually.

- The Remedy: This mismatch creates a severe financial illusion, resulting in a project that looks highly profitable on a spreadsheet but completely destroys real purchasing power upon maturity. Financial teams must strictly match their parameters: if you project nominal cash flows, apply a nominal discount rate; if you project real cash flows, adjust your discount rate to remove inflation.

Pitfall 3: Distorting the Timing of Cash Inflows

- The Issue: Modeling an investment under the simplistic assumption that all cash returns materialize cleanly at the very end of the fiscal year (Year-End Convention), when in reality cash flows enter the company continuously or at the beginning of the period.

- The Remedy: Miscalculating these timing dynamics causes severe valuation distortions. By underestimating or overestimating present value by even a slight margin, an enterprise can easily pass an excellent strategic opportunity directly to a competitor, or worse, greenlight an unprofitable project.

5. Executive Action Guide: The Key to Corporate Optimization

To successfully integrate the time value of money into macro-level corporate governance, the CEO must maintain a strict, cash-centric perspective that looks past short-term financial reporting metrics.

- Enforce Aggressive Hurdle Rates During Monetary Contraction: In periods of economic slowdown or high-interest-rate environments (such as the current conditions of 2026), immediately raise your corporate discount rate benchmarks. This structural adjustment tightens your capital gates, blocking unnecessary cash outlays and filtering for truly elite investment options.

- Continuously Audit Net Working Capital Multipliers: An investment can present an exceptional net present value on paper, but if it locks up enterprise liquidity in massive inventory lines or raw materials for extended cycles, it can trigger a sudden cash crunch. Always verify your liquidity buffers alongside your present value metrics.

CEO Memo: Executing capital investments without factoring in the time value of money hands control of your enterprise over to future uncertainty. Implementing a rigorous present value architecture and a dynamic discount rate framework is your primary mechanism to mitigate long-term risk while systematically multiplying corporate value.

Corporate Catchphrase: “Financial projections that ignore time erode corporate capital; meticulous present value analysis locks in long-term wealth.”

Conclusion: Key Takeaways

- Time is a Cost: Never evaluate long-term corporate projects using simple nominal sums. A dollar received tomorrow will never carry the economic power of a dollar deployed today.

- Differentiate Your Hurdles: Adjust your discount rates dynamically based on project duration and localized risk exposures to protect the enterprise against long-term suboptimization.

- Maintain Cash Fidelity: Base all present value calculations on verified, after-tax cash movements rather than flexible accounting net income targets.