In our previous discussion, we explored how process costing works like a pipeline, averaging the costs across an entire production stage rather than tracking individual receipts. But a practical question often arises in the real world.

Imagine you are running a production line for a craft soda brand or a premium snack company. You produce four different flavors—say, Classic, Spicy, Diet, and Lime—all using the same base process but with slightly different additives. Since the product names are different, should you revert to complex Job Costing? Today, we dive into the strategy for managing costs in these “blended” product families, starting from the bedrock principles of inventory recording.

1. Similar Product Lines: Job Costing or Process Costing?

Whether it is four types of Ramen or a variety of flavored energy drinks, these products often share a core manufacturing “DNA.” They might use the same mixing vats, the same bottling lines, and the same cleaning cycles. Because these items have a low unit cost and are produced in massive volumes, creating a separate “job jacket” or ledger for every single unit—the hallmark of Job Costing—is grossly inefficient.

Instead, these businesses maintain the framework of Process Costing but utilize a specialized sub-type known as Class Costing (or Operation Costing). This allows managers to maintain the speed of mass-production accounting while still reflecting the subtle differences between product variations.

2. What is Class Costing?

Definition: Class costing is used when products are produced from the same raw materials through the same basic processes but result in different specifications, such as shape, size, weight, or quality.

The Magic of Equivalence Coefficients: This is the secret sauce. Managers assign a “weight” or index to different products based on their relative resource consumption. For example, a “Standard” snack might be 1.0, while a “Premium” version with more expensive seasoning might be assigned a coefficient of 1.2.

The Limitations: This method relies heavily on the accuracy of these coefficients. If the coefficients are set subjectively or if the production processes diverge significantly, the cost data becomes distorted.

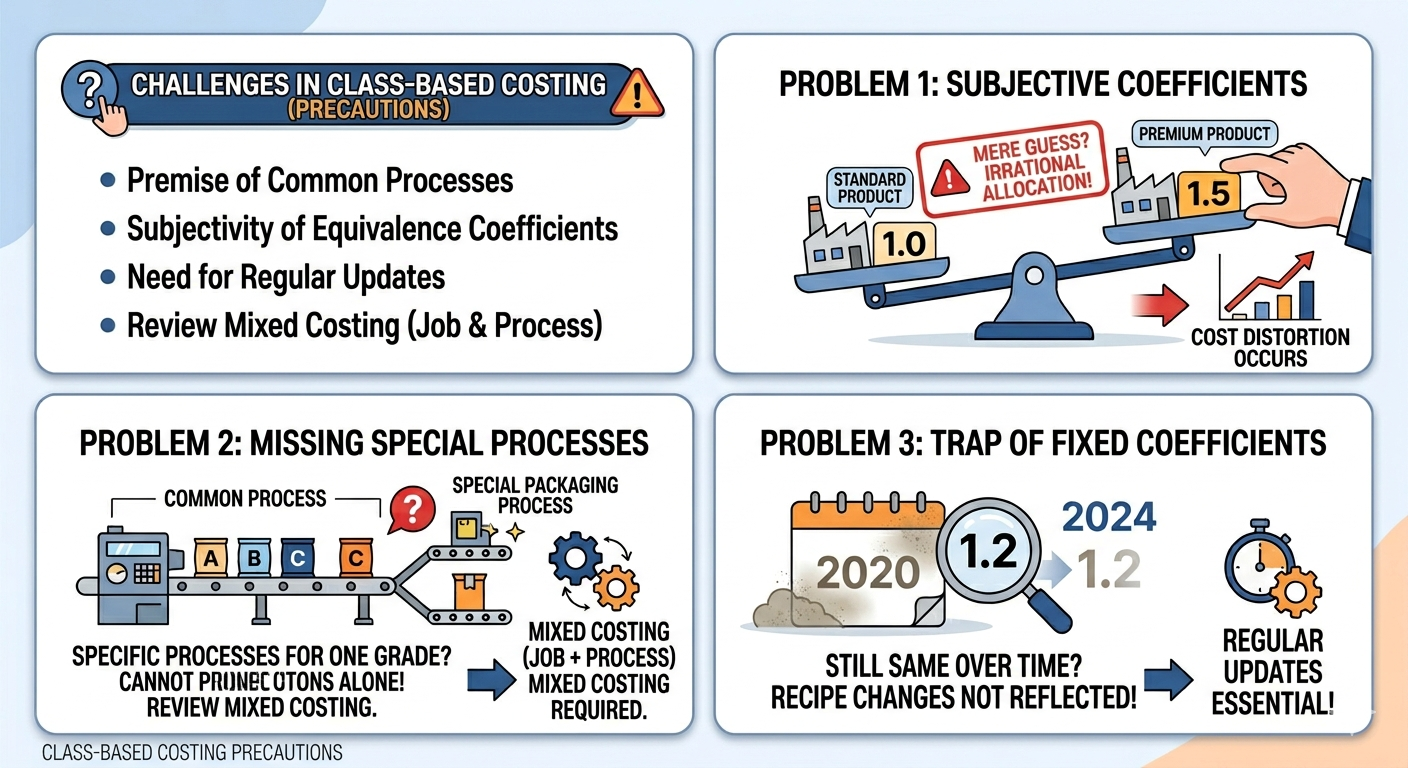

Critical Considerations for Implementation

- Verify Process Homogeneity: Class costing assumes a “shared journey.” If a premium line requires a specialized, high-tech finishing stage that the standard line does not, you cannot rely on a simple coefficient. You must apply a Hybrid Costing approach: use class costing for the shared stages and direct charging for the specialized stage.

- Objective Equivalence Coefficients: This is the most vital step. You cannot simply say, “It’s a luxury item, so let’s multiply by 1.5.” You must use physical metrics like weight, volume, mixing time, or ingredient ratios. If these are inaccurate, one product will end up “subsidizing” the other, leading to poor pricing strategies.

- Periodic Updates: Recipes and machine efficiencies change. Using a coefficient from three years ago is a recipe for financial disaster. Regular monitoring is required to ensure the index still reflects the reality of the factory floor.

- Handling Spoilage and Defects: In mass production, “spoilage” is inevitable. You must determine if defects occur equally across all classes. If the “Premium” line has a much higher failure rate due to its complexity, those losses should be assigned specifically to that line rather than being averaged across the “Standard” products.

- Market Value Alignment: Always check your calculated costs against the Net Realizable Value (NRV). If your allocation logic results in a product cost that is higher than its selling price, your allocation base might be fundamentally flawed.

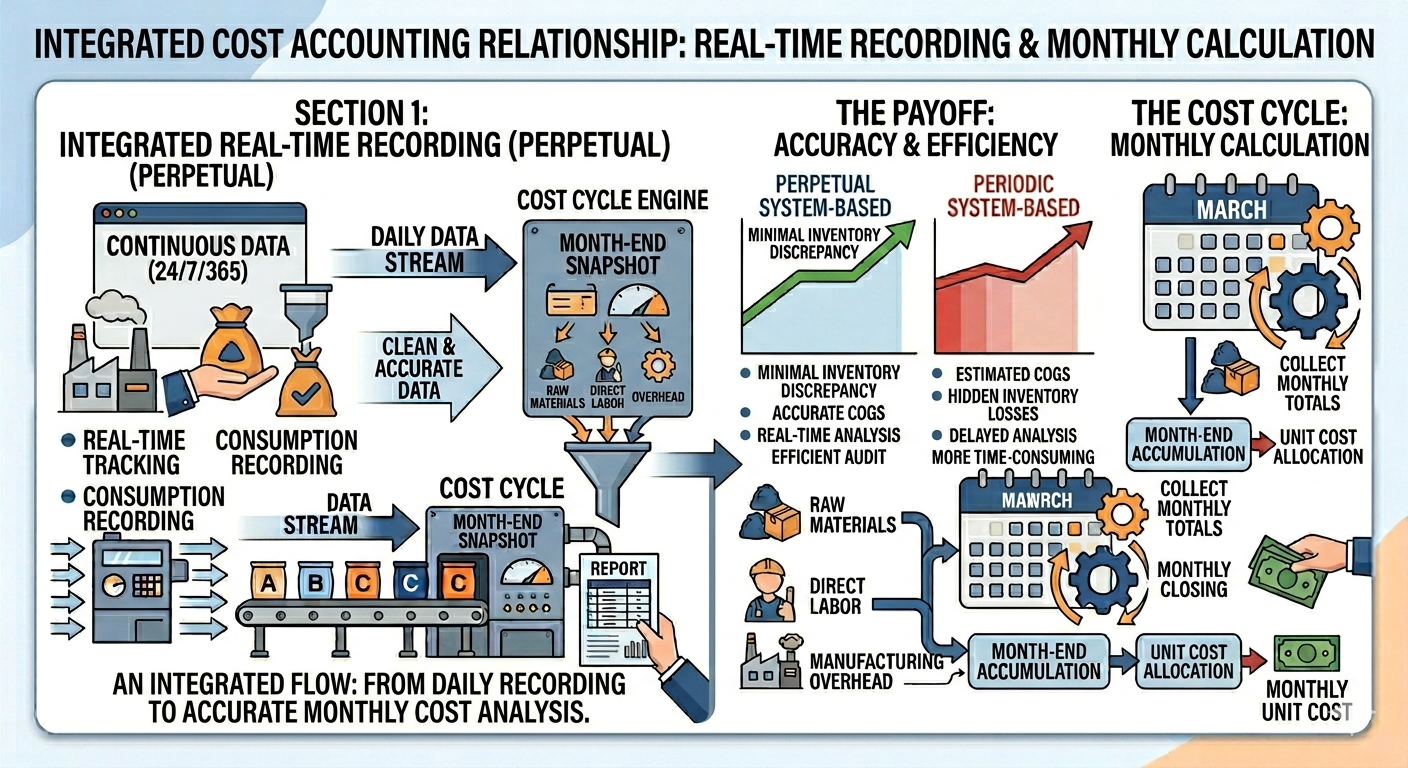

3. The Foundation of Accuracy: Why You Must Use a Perpetual Inventory System

Class costing and cost allocation are essentially “division problems” performed at the end of a period. However, if the “numerator” (the total cost of materials used) is wrong, the entire result is a lie. This is why a Perpetual Inventory System is non-negotiable for modern management.

The Dangers of the Periodic System

Under a Periodic Inventory System, you only count what is left at the end of the month and work backward. The danger here is that any inventory that was stolen, evaporated, or spoiled is automatically hidden within the “cost of production.” You end up treating waste as if it were a useful ingredient in your products.

The Necessity of the Perpetual System

- Real-Time Visibility: By recording every inflow and outflow as it happens, you can immediately identify “shrinkage” or process inefficiencies.

- Data Integrity: You need a high-fidelity “Flow of Quantities” to apply equivalence coefficients effectively. If you lose track of the physical flow, your month-end cost allocation loses all credibility.

| Feature | Perpetual System | Periodic System |

| Tracking | Real-time recording of every transaction | Backward calculation based on year-end count |

| Advantage | Immediate identification of waste/loss | Low administrative cost and effort |

| Analogy | Real-time banking app notifications | Checking your balance once a month |

4. The Rhythm of Costing: Monthly Cycles and Year-End Adjustments

While recording happens every day (Perpetual), the final unit cost is usually calculated in Monthly Cycles. This is because utility bills and labor payrolls are typically finalized at month-end.

- Data Collection (Perpetual): Real-time tracking forms the “muscle memory” of your costing system.

- Costing Cycle (Monthly & Annual): Costs like electricity or indirect labor are allocated at the end of the month to determine the average unit cost.

- Allocation Logic (Coefficients): Weights are applied to the gathered data to ensure fair distribution among the various product classes.

5. Strategic Takeaways for Managers

To master the production of similar product lines, focus on these two pillars:

- Refine Your Coefficients: Constantly ask if your weights (weight, time, etc.) truly explain the difference in costs between your “Classic” and “Premium” lines.

- Embrace the Time Gap: Understand that while recording must be a high-resolution, real-time activity (Perpetual), valuation is a periodic, strategic activity. Closing this gap is how you ensure your financial reports reflect the truth of your operations.

Conclusion: Key Takeaways

- Efficiency over Complexity: Use Class Costing for similar products to avoid the administrative nightmare of Job Costing.

- Accuracy via Perpetual Tracking: Real-time inventory records are the only way to ensure the costs you are allocating are accurate and free from “hidden” waste.

- Consistency and Vigilance: Regularly audit your equivalence coefficients to ensure they reflect current production realities and recipe changes.

AI Disclosure: Created in collaboration with Google Gemini. All core content was authored, reviewed, and edited by the author.