When processing a single steer in agricultural production, you simultaneously obtain ribeye steaks, tenderloins, and hide. How should the corporate accountant distribute the baseline ranching and operational expenses across these distinct end products? This puzzle introduces the core challenge of Joint Cost Allocation.

In corporate financial management, tracking expenditures when multiple outputs emerge from a single operational source is a foundational requirement. In 2026, navigating this distribution cleverly has evolved beyond basic compliance or mere bookkeeping. Today, it serves as a critical strategic lever that corporate executives use to identify hidden margins, optimize product pricing, and uncover structural efficiency. This guide breaks down the mechanics of transforming shared overhead into actionable financial data.

1. Grounding the Concept: Everyday Analogies and Core Definitions

To fully grasp the mechanics of joint costs, look at an example common in North American retail: creating a premium fruit basket assortment.

Imagine purchasing a large, wholesale bulk pallet containing apples, pears, and grapes mixed together. Because you paid a single upfront invoice for the entire pallet, assigning an exact, unvarnished acquisition price to each distinct fruit variety requires a systematic formula.

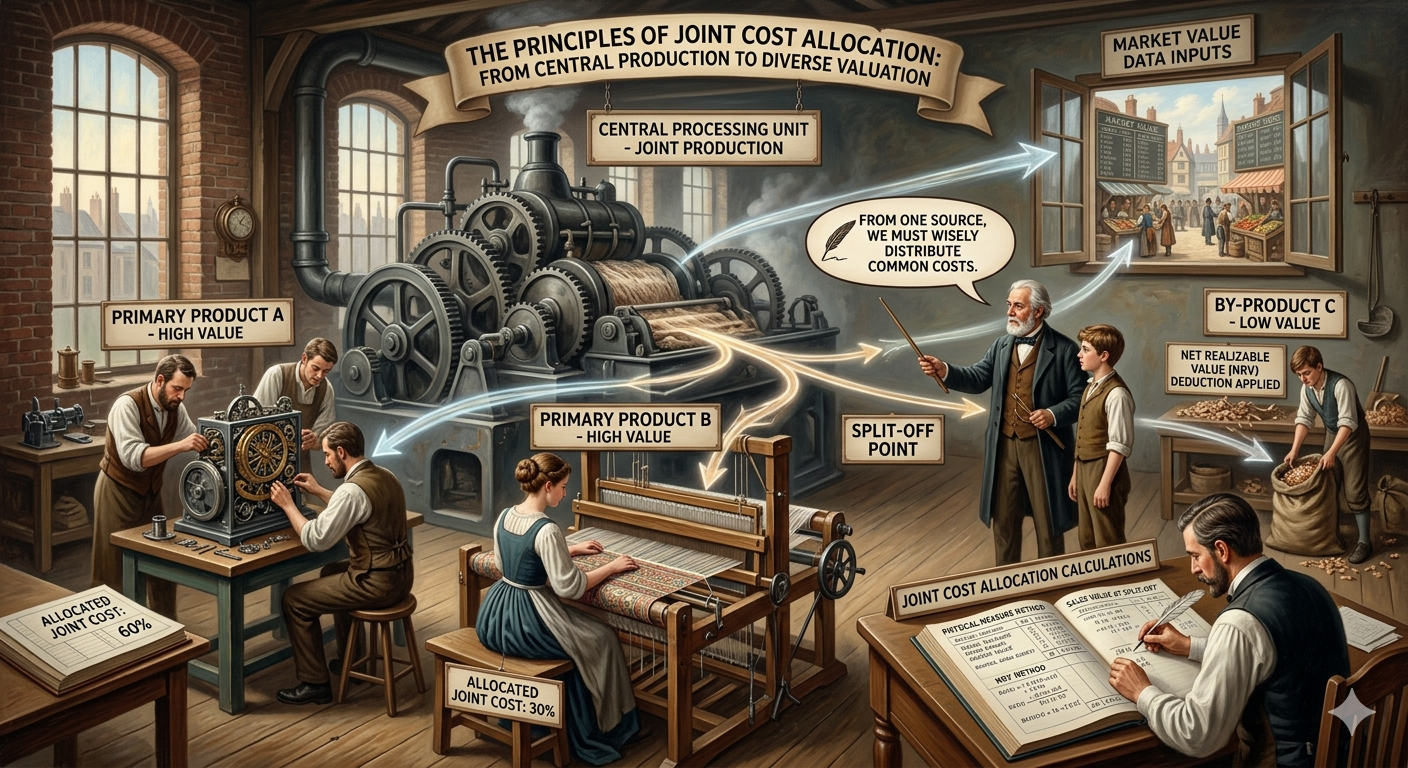

① Joint Cost Allocation

- Joint: This denotes a single, unified operational framework where multiple independent assets are structurally linked during the initial phase of processing.

- Cost: The total capital and manufacturing overhead deployed to execute the production process.

- Allocation: The mathematical distribution of shared expenditures to individual segments using objective, reliable metrics.

- Comprehensive Meaning: This is the managerial accounting framework used to distribute shared upstream expenditures among distinct corporate outputs that are created simultaneously within a single manufacturing or refining process. Classic industrial examples include petrochemical refining (where crude oil yields gasoline, diesel, and jet fuel simultaneously) or large-scale poultry processing lines.

② Core Terms You Must Know

Navigating this financial landscape requires a clear understanding of four foundational architectural milestones:

- Joint Products: These represent two or more distinct outputs generated simultaneously from a single raw material input and processing line. Crucially, each product holds significant commercial value, meaning management cannot treat any of them as a simple waste stream. Every joint product is a primary driver of top-line revenue.

- Split-off Point: This is the exact operational milestone where the shared manufacturing process diverges. At this point, the intertwined joint products become physically identifiable as separate, individual assets. All expenditures accumulated prior to this milestone constitute the total joint cost.

- Separable Costs: These represent any individual manufacturing or refining expenditures incurred after the split-off point. Because these costs are deployed exclusively to enhance a single, specific product line after it has emerged independently, they are traced directly to that specific asset without any complex allocation formulas.

- By-products: These are secondary outputs of minor commercial significance that emerge incidentally during the manufacturing of primary joint products. For example, when harvesting beef, the primary meat cuts are the joint products, whereas the bone fragments or residual tallow represent by-products.

2. The Three Allocation Pillars: Advantages and Pitfalls

To distribute accumulated shared upstream costs down to individual products at the split-off point, corporate accountants rely on three standard mathematical methodologies.

① The Physical Measures Method

This approach allocates shared upstream expenditures based strictly on physical volume, mass, or quantity metrics recorded at the split-off milestone.

- Advantages: It delivers a completely objective, easily auditable calculation framework that is entirely decoupled from external market dynamics.

- Limitations: It completely ignores variations in asset value. For example, if an industrial mining operation extracts a single ton of material containing both high-value precious metals and low-value industrial copper, this method applies identical per-pound production costs to both. This can lead to distorted margin reports.

② The Sales Value at Split-off Method

This method allocates shared joint costs based on the relative market value of each product at the exact moment they split into separate streams.

- Advantages: It matches costs with revenue-generating capacity. Higher-value products absorb a larger share of the initial expenses, keeping product profit margins stable.

- Limitations: It depends heavily on active liquid markets at the split-off point. If a product has no established market price at that stage and requires further processing to become salable, this method cannot be used cleanly.

③ The Net Realizable Value (NRV) Method

The NRV approach calculates a hypothetical value for products that cannot be sold at the split-off point. It takes the final expected selling price and subtracts all downstream separable processing and marketing expenses.

$$NRV = \text{Final Market Value} – \text{Separable Downstream Costs} – \text{Selling Expenses}$$

- Advantages: It provides a reliable framework for evaluating complex, multi-stage production lines, ensuring that downstream processing decisions are grounded in actual product profitability.

- Limitations: It requires continuous estimation of future processing costs and final market values. If downstream operational costs spike unexpectedly, the upstream cost allocation shifts, introducing volatility into your financial reporting.

3. Three Critical Strategic Issues and Advanced Data Solutions

Managing joint operations involves navigating complex financial trade-offs. Modern accounting relies on clear financial logic and data automation to solve these three common friction points:

① The Incremental Processing Fallacy

- The Issue: Many corporate managers make the mistake of including allocated joint costs when deciding whether to process a product further or sell it immediately at split-off. This can lead to poor decision-making and missed profits.

- The Solution: Upstream joint costs are completely sunk. Once incurred, they cannot be recovered and are entirely irrelevant to future operational decisions. Management should focus exclusively on Incremental Logic: process further if, and only if, the additional revenue gained exceeds the extra downstream costs. Modern ERP platforms run continuous marginal simulations to highlight the exact milestone where further processing stops adding value.

② Ambiguity in By-product Valuation

- The Issue: Allocating a standard portion of shared costs to low-value by-products can artificially deflate their margins and distort the true cost structure of your primary products.

- The Solution: Use the Production Method. Under this approach, the net realizable value of by-products is estimated when they are created and subtracted directly from the total joint cost pool. This isolates and protects the cost integrity of your primary revenue drivers. Furthermore, many North American companies use sustainability data to turn these waste streams into valuable eco-friendly materials, reclassifying them from simple by-products to secondary joint products.

③ Arbitrary Allocation and Internal Conflict

- The Issue: Because choosing an allocation method is ultimately a management policy choice, it can create internal friction. Shifting methods can make one division look highly profitable while turning another net-negative, sparking internal political debates over performance bonuses.

- The Choice of the Constant Gross Margin Method: To mitigate this friction, corporate leaders often use the Constant Gross Margin Percentage Method. This framework works backward to allocate joint costs so that every single joint product yields an identical gross margin percentage. By ensuring that no single product line appears artificially unprofitable due to shared expenses, it provides organizational fairness and simplifies performance reviews.

4. Financial Planning and Leadership Strategies

In today’s fast-paced corporate environment, data automation plays a transformative role. Advanced enterprise systems connect live commodity market pricing with real-time supply chain data. Rather than relying on frozen, historic cost assumptions, modern systems dynamically recalculate product values based on expected market conditions at the exact time of delivery.

When choosing a long-term allocation framework, financial leaders should align their accounting policies with their broader corporate goals:

- The Stability-First Strategy: For companies operating in highly volatile raw commodity markets, using the Physical Measures Method provides a steady, predictable cost foundation that keeps baseline financial reporting consistent.

- The Growth-Oriented Strategy: For executives focused on expanding product lines or maximizing asset valuations, using the Net Realizable Value (NRV) Method is highly effective. It delivers the granular, forward-looking insights needed to decide exactly which products to process further, maximizing overall profitability.

5. Quick Reference: Allocation Methodology Summary

| Evaluation Category | The Physical Measures Method | The Sales Value Method | The Net Realizable Value Method |

| Core Allocation Metric | Volumetric / Mass Units (e.g., lbs) | Spot Market Price at Split-off | Estimated Final Net Margin |

| Operational Focus | Simplicity and objectivity | Current revenue capacity | Future value optimization |

| Target Industries | Mining, basic refining, agriculture | Meat packing, bulk chemicals | Pharmaceuticals, specialty tech |

Conclusion: Key Takeaways for Today’s Corporate Leaders

Managing joint cost allocation effectively requires shifting from passive compliance to proactive capital management.

- Isolate Sunk Costs: Never allow upstream joint costs to cloud your downstream processing decisions. Base further processing choices strictly on incremental revenues and expenses.

- Neutralize Performance Biases: Recognize that joint cost allocation contains an inherent element of choice. Select a method that prevents internal corporate friction and matches how your division managers are evaluated.

- Automate Your Visualizations: Move away from static spreadsheets. Use modern financial systems to track market fluctuations in real-time, turning your accounting models into dynamic tools for corporate strategy.

AI Disclosure: Created in collaboration with Google Gemini. All managerial accounting principles, joint cost allocation methodologies, and corporate decision-making frameworks were co-authored, technically audited, and verified by the author to ensure complete structural alignment with modern corporate wealth management standards and US GAAP financial reporting guidelines.