Have you ever imagined what the world of investing would look like without Exchange Traded Funds (ETFs)? Before their rise, if you wanted to invest in the U.S. semiconductor market, you would have had to manually analyze and purchase dozens of individual stocks. If you didn’t have enough capital, true diversification was a distant dream. Furthermore, withdrawing money from a traditional mutual fund often meant waiting a week for the transaction to clear. In short, investing was often synonymous with “pain.”

Today, we dive deep into the crown jewel of modern finance that saved us from this hassle—the ETF—and its slightly more complex cousin, the ETN.

1. The Core Philosophy: Why the Hype?

The ETF is the ultimate realization of Index Theory: “Don’t try to beat the market; capture the market’s return.” By bundling hundreds of stocks, ETFs virtually eliminate “unsystematic risk” (such as a single company going bankrupt). They revolutionized liquidity by allowing these bundles to be bought and sold in real-time, just like a single share of Apple or Microsoft.

2. Anatomy of the Terms: The Answer is in the Name

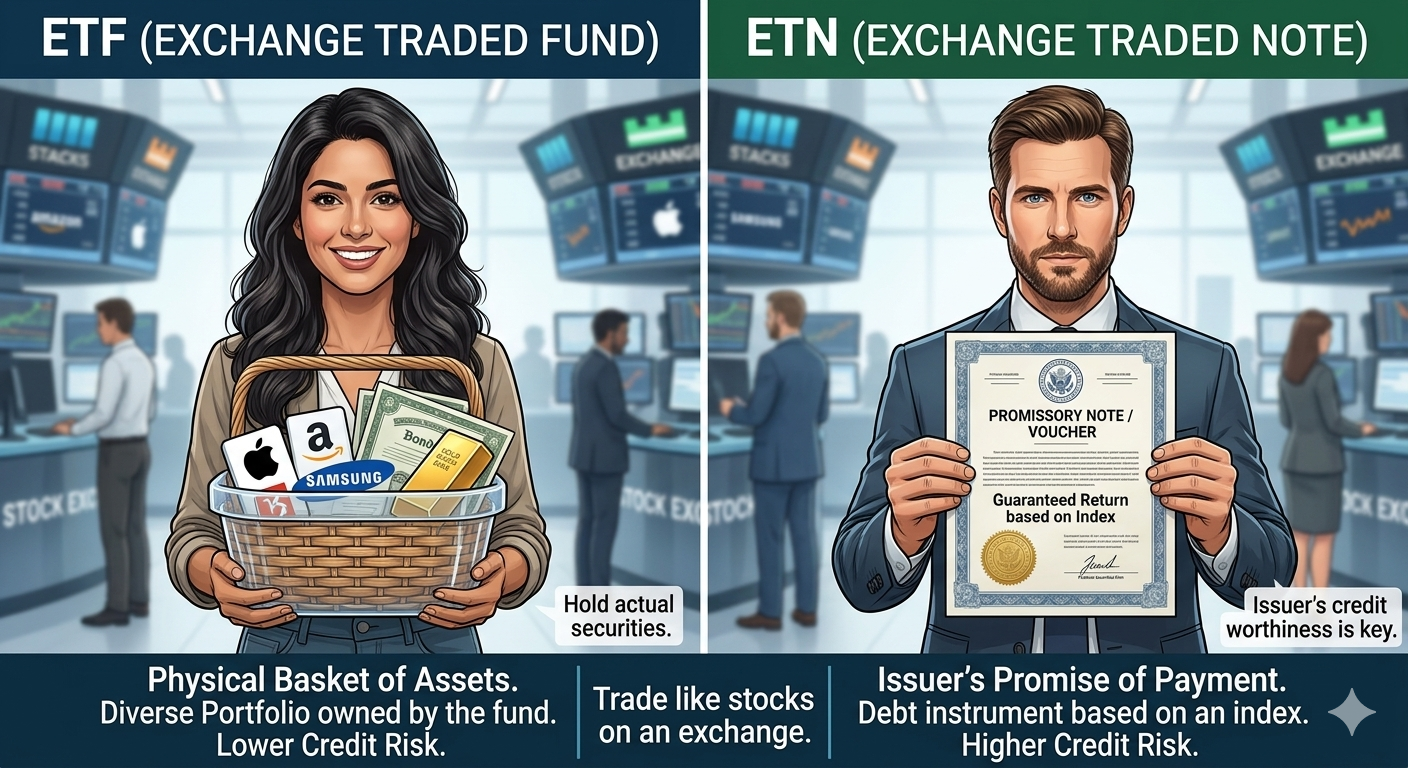

1) ETF (Exchange Traded Fund)

- Exchange Traded: This means you can buy and sell it on the stock market as easily as buying groceries at a supermarket.

- Fund: A “basket” where experts have gathered various stocks using pooled money from many investors.

- The Bottom Line: A “Gift Basket” of stocks that trades with the ease of a single share.

2) ETN (Exchange Traded Note)

- Exchange Traded: Same as above. You buy it instantly via your brokerage app.

- Note: This is not a basket. It is a “promissory note” or a “IOU” issued by a financial institution (usually a bank or brokerage).

- The Bottom Line: A “Contract” where a bank promises to pay you a return based on an index.

3. The Perfect Analogy: “The Bento Box” vs. “The Meal Voucher”

If the technical terms are still a bit foggy, remember this simple comparison:

- ETF is a “Bento Box.” Inside the box, the ingredients—the salmon, the rice, the greens (representing Nvidia, Tesla, or JPMorgan)—actually exist. Even if the restaurant (the fund manager) goes out of business, the ingredients are still held safely in the kitchen (the custodian bank). Your meal is secure.

- ETN is a “Gourmet Meal Voucher.” You don’t actually hold the food in your hands. Instead, you hold a piece of paper. The restaurant (the bank) promises: “When you redeem this, we will pay you the exact cash value of that Bento Box.” You have to trust that the restaurant stays in business to honor that voucher.

4. Real-World Examples for Clarity

How do these look in a typical North American brokerage account?

- Example of an ETF: “Vanguard S&P 500 ETF (VOO)”This basket contains the actual shares of the 500 largest companies in the U.S. When you buy one share of VOO, you effectively become a tiny owner of 500 powerhouse corporations simultaneously. It is a basket filled with real assets.

- Example of an ETN: “iPath Series B Bloomberg Cotton Subindex Total Return ETN (BAL)”Storing physical cotton is difficult and expensive. Instead, a bank issues a “Note.” They promise that if cotton prices rise by 1%, they will pay you exactly 1% profit. You don’t own a bale of cotton; you own the bank’s promise to pay you based on cotton’s performance.

5. If Returns are Guaranteed, is the ETN Better?

It might sound tempting, but there is a catch. The “guarantee” refers to the calculation, not the safety of your principal if the issuer collapses.

1) The Meaning of ‘Guaranteed Return’: Calculation Accuracy

ETNs win on precision. Because it’s a contractual promise, if the index moves 1%, the bank pays 1%. ETFs, because they have to physically buy and sell stocks, incur trading costs and taxes that can cause a tiny “tracking error” (e.g., the index moves 1%, but the ETF moves 0.98%).

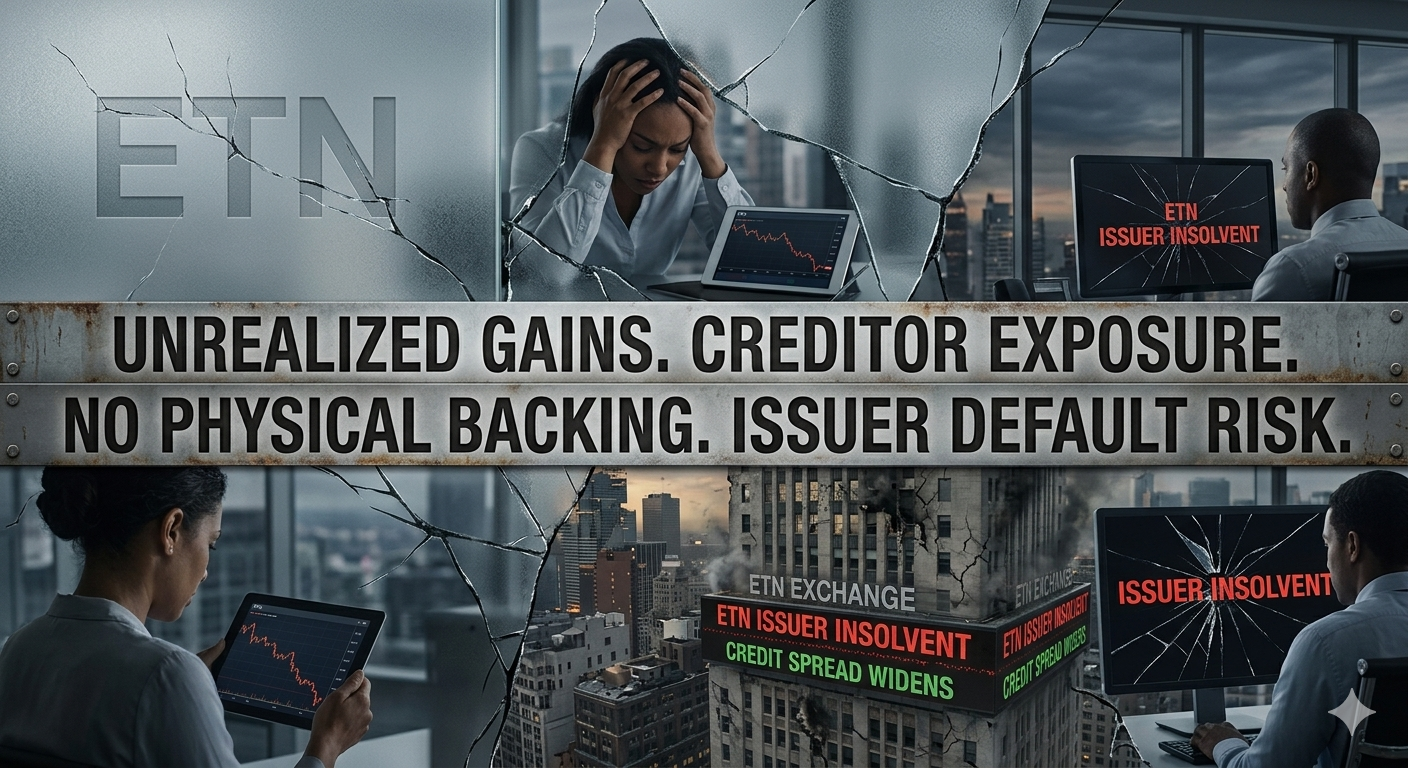

2) The Shadow of ‘Credit Risk’

This is the deal-breaker for many. An ETN is only as good as the bank that signed it.

- ETF (Bento Box): If the manager goes bankrupt, the stocks in the vault still belong to you.

- ETN (Meal Voucher): If the bank fails, your voucher becomes a useless piece of paper.

- Historical Lesson: During the 2008 financial crisis, when Lehman Brothers collapsed, investors holding ETNs issued by Lehman lost everything. The “note” became worthless because the promisor disappeared.

3) The Expiration Date (Maturity)

You can hold an ETF for generations and pass it to your children. ETNs, however, usually have a maturity date (ranging from 1 to 20 years). For long-term “set it and forget it” investors, ETFs are far more convenient.

6. Summary: Safety vs. Precision

| Category | ETF (The Basket) | ETN (The Note) |

| Biggest Strength | Safety! Your assets are protected even if the manager fails. | Precision! Zero tracking error and access to exotic markets. |

| Biggest Weakness | Small “tracking errors” due to trading costs. | Credit Risk! If the bank goes under, your money is gone. |

7. Practical Strategy: Which One Should You Buy?

1) Choose an ETF if:

- Safety is your priority: You want to sleep soundly knowing your assets are held in a third-party vault.

- You are a long-term investor: You want to hold an investment for decades without worrying about maturity dates.

- Retirement Planning: You are investing in a 401(k) or IRA and want stable, asset-backed growth.

- Recommended: VOO (S&P 500), VTI (Total Stock Market).

2) Choose an ETN if:

- You demand 100% accuracy: You cannot tolerate even a 0.01% deviation from the index.

- You want to trade Commodities or Volatility: You are looking for exposure to things that are hard to “store,” like carbon credits, cocoa, or specific oil futures.

- You are a short-term tactical trader: You trust the credit of a major bank (like JPMorgan or Barclays) for a short-term play to maximize precision.

- Recommended: Commodity-linked notes or specific thematic sector notes.

Conclusion: Key Takeaways

- Core Difference: ETFs are backed by physical assets; ETNs are backed by the credit of a bank.

- Security: ETFs offer superior protection against institutional failure.

- Accuracy: ETNs offer better tracking of difficult-to-reach markets but come with an expiration date.

- Investment Strategy: For 90% of retail investors, ETFs are the standard choice for building long-term wealth safely.

AI Disclosure: Created in collaboration with Google Gemini. All core content was authored, reviewed, and edited by the author.