Modern manufacturing—spanning industries from semiconductors and automotive assembly to chemical processing—operates through a complex web of intermediate stages. In this environment, each stage functions as an independent Cost Center.

If a company fails to manage costs at each specific stage and instead attempts to calculate everything only at the final finish line, they lose the ability to accurately value Work-in-Process (WIP)—the unfinished goods sitting on the factory floor. This leads to a distortion of asset values and critical errors in executive decision-making. Therefore, understanding how costs migrate and accumulate between processes is the essential starting point for precise profitability analysis.

1. Understanding Transferred-In Costs: The Foundation of Sequential Production

When multiple production stages are linked, the costs incurred in the first stage and moved to the second are known as Transferred-In Costs.

The Unique Timing of Inputs

From the perspective of the second department, Transferred-In costs are considered 100% complete and added at the very beginning of the process. This is because the item arrives having already undergone all necessary labor and material additions from the previous stage.

The Cumulative Nature

Think of this as a “snowball effect.” As a product moves through each successive department, the costs from previous stages continue to stack, creating a cumulative financial burden that represents the total resources consumed up to that point.

2. The Mechanics of a Three-Stage Cost Flow

In a three-stage manufacturing environment, cost calculation occurs independently at each center, with the results “delivered” to the next stage like a relay race.

1) The Level-by-Level Breakdown

- Stage 1 (Base Level): Costs for direct materials and conversion are calculated using standard equivalent unit methods to determine a unit cost. This “Finished Goods Cost” for Stage 1 becomes the “Starting Point” for Stage 2.

- Stage 2 (Subsequent Level): The cost elements expand into three categories: ① Transferred-In Costs, ② Current Stage Materials, and ③ Current Stage Conversion Costs. Regardless of the physical progress in Stage 2, the Transferred-In cost is applied at 100% to any ending WIP.

- Stage 3 (Final Assembly): Stage 3 follows the same logic as Stage 2. However, its “Transferred-In” component now represents the combined accumulated value of both Stages 1 and 2.

2) The Core of Equivalent Unit Calculations

- Progress of Transferred-In Costs: Regardless of whether Stage 3 is only 10% complete in terms of its own labor, the units in that stage have already survived 100% of the work from Stages 1 and 2. Thus, for equivalent unit calculations, Transferred-In costs are always assigned 100% completion.

- Current Stage Costs: Materials are accounted for based on their specific point of injection, while conversion costs (labor/overhead) are allocated based on the actual percentage of work performed within that specific stage.

3. Real-World Application and the Dangers of Mismanagement

Consider the assembly of a smartphone in a North American tech hub.

- Process A (Mainboard Assembly): Raw materials (chipsets, etc.) and assembly labor are invested to create a mainboard with a unit cost of $400.

- Process B (Final Assembly): This stage receives the $400 mainboard (Transferred-In) and adds a display screen ($200) and final assembly labor ($50).

- The Correct Result: The final product cost is accurately calculated as $650 ($400 + $200 + $50).

The Catastrophic Risks of Ignoring Transferred-In Costs

If a manager only tracks the $250 added during the final assembly and fails to accumulate the $400 from the previous stage, the following “Management Disasters” occur:

- Lack of Traceability: If the final cost spikes, you won’t know if the culprit is the chipset price in Process A or the display yield in Process B. You lose the ability to pinpoint the Source of Inefficiency.

- Inventory Understatement: If you have 1,000 smartphones in the warehouse valued at $650,000 but only record them at $250,000 on the books, your financial statements become fundamentally unreliable. This is a major accounting failure.

- Pricing Strategy Failure: If you see a “book cost” of $250 and set a sale price of $500, you are actually losing $150 per unit. This leads to “Profitable Insolvency”—where a company appears to be selling well but is actually bleeding cash toward bankruptcy.

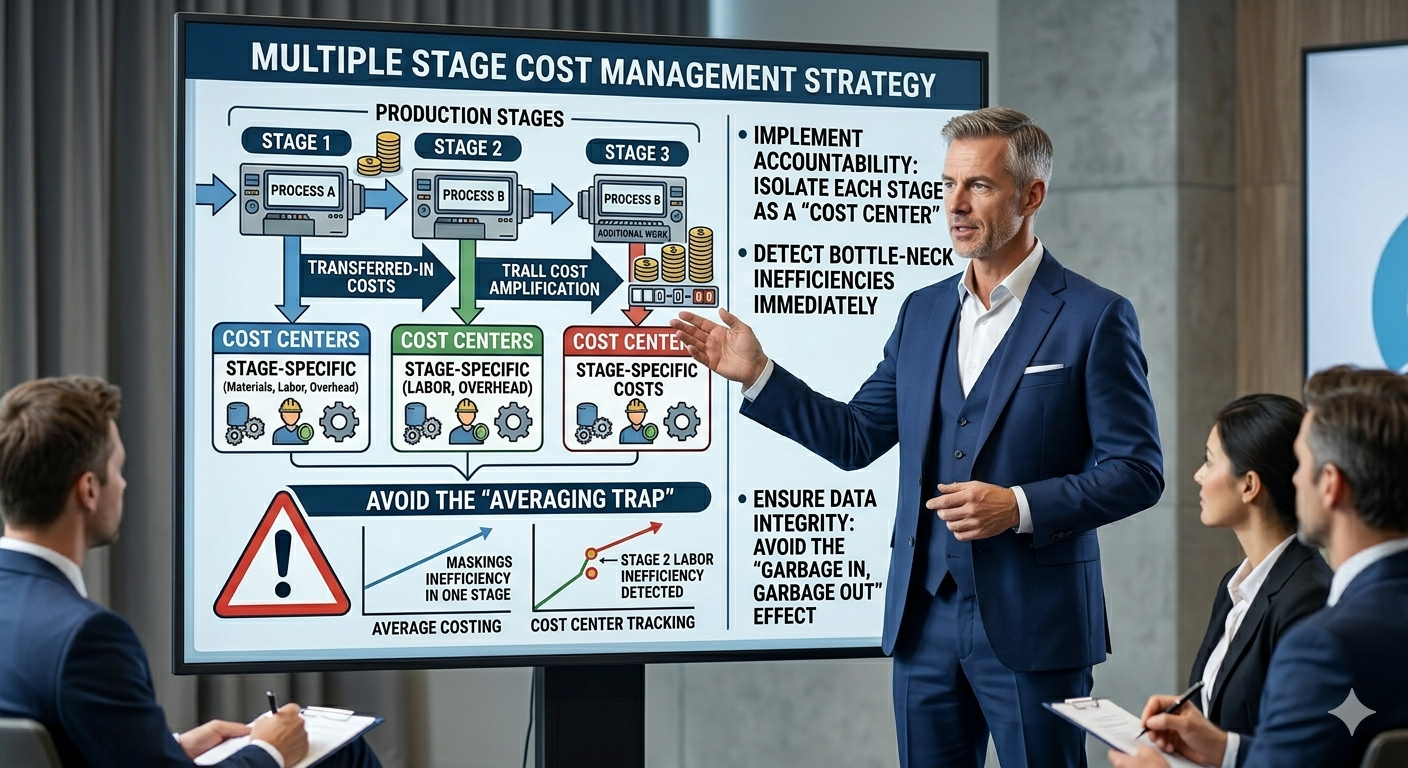

4. Control Strategies for Multi-Stage Environments

Management must realize that costs “amplify” at every gate. Precision in WIP valuation is the only guardrail against total financial distortion.

Responsibility Accounting and Performance Evaluation

Setting each process as an independent Cost Center clarifies where capital is being wasted. If final costs rise, you must be able to immediately distinguish between a raw material hike in the first stage and an efficiency drop in the second. Without this separation, inefficiencies are hidden by the “Trap of Averaging.”

Analyzing Bottleneck Cost Drivers

In multi-stage setups, a bottleneck in one department traps all the Transferred-In costs from previous stages in that specific area. Managers must monitor the gap between equivalent units and physical units to ensure that too much capital isn’t “locked” in the production line, creating a high opportunity cost.

The Domino Effect of Data Integrity

Process costing is a domino structure where the output of one stage is the input of the next. “Garbage In, Garbage Out.” An error in the very first stage’s count or progress estimation will contaminate every subsequent stage, leading to a completely falsified final unit cost report.

Conclusion: Key Takeaways

- The Accumulation Principle: Transferred-In costs are the accumulated financial “DNA” of a product, growing as it moves toward completion.

- The 100% Rule: For accounting purposes, Transferred-In costs are always 100% complete at the start of a new department, regardless of that department’s specific progress.

- Management Vigilance: Accurate tracking prevents inventory understatement and suicidal pricing strategies, ensuring that “profitable” sales are actually generating cash.

AI Disclosure: Created in collaboration with Google Gemini. All core content was authored, reviewed, and edited by the author.