In our previous exploration, we established the bedrock of accounting: the definition of “Cost” and the three fundamental elements of manufacturing. However, the intellectual journey of a manager does not stop there. A critical question inevitably arises: “Product A and Product B follow completely different manufacturing paths and consume entirely different materials—is it truly accurate to calculate their costs using a single, broad average?”

Whether it is a custom-tailored suit for a high-profile client, a multi-billion dollar aerospace project like a SpaceX rocket, or a massive global branding campaign for a tech giant—these “one-of-a-kind” projects require a surgical level of tracking. This precision instrument is known as Job Order Costing. Today, we will deconstruct the mechanisms of Job Order Costing that complete the finer details of business strategy.

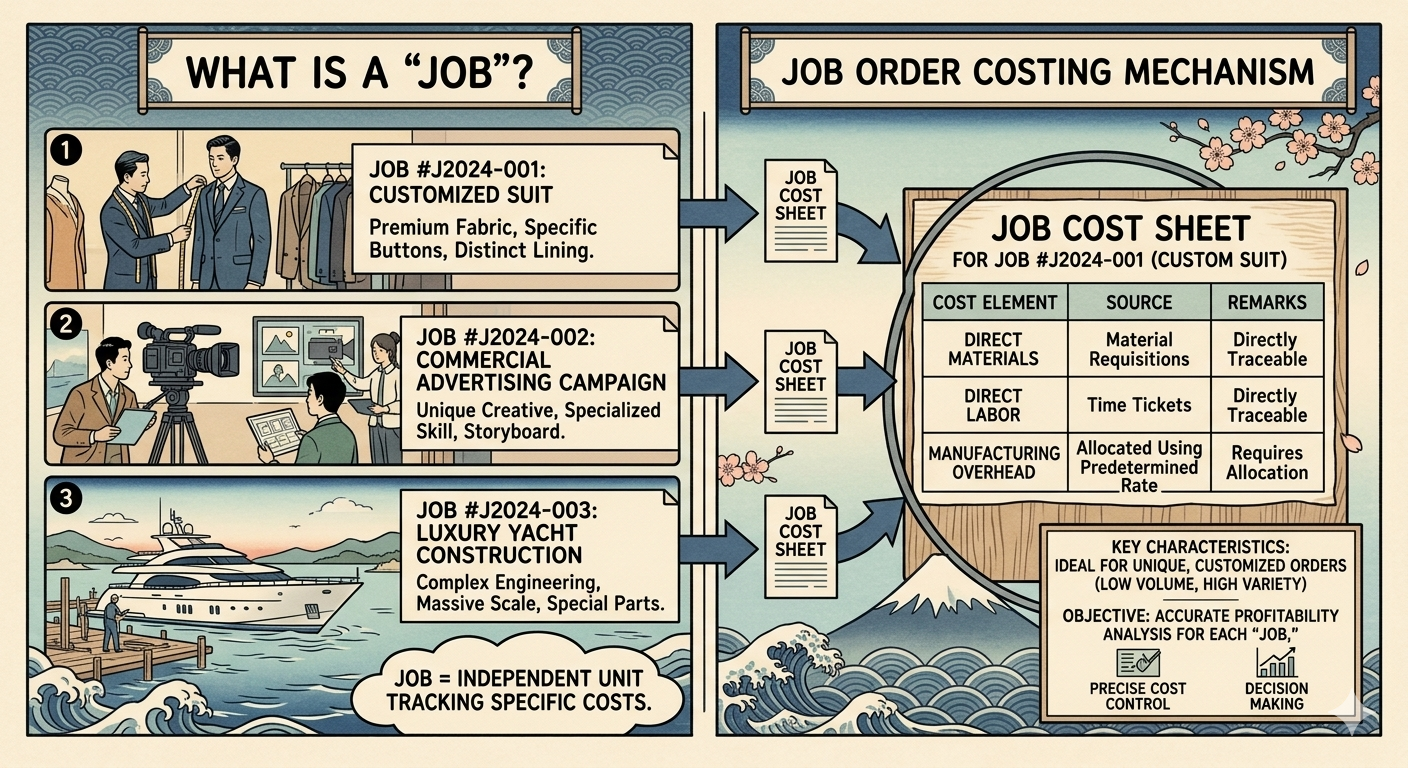

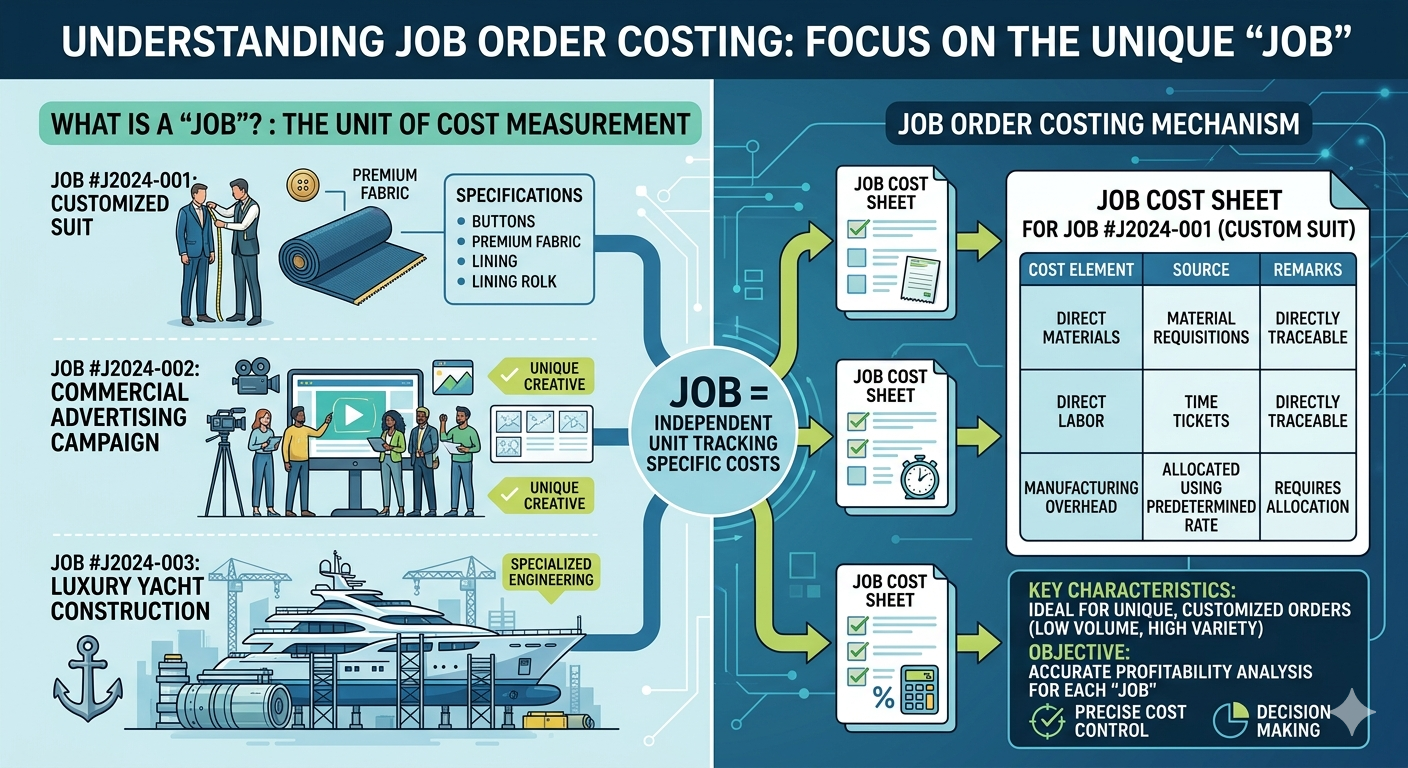

1. What is a “Job”?: The Fundamental Unit of Costing

All meaningful measurement begins with defining the subject. In this system, a “Job” is not merely a task or a piece of work; it is the independent unit used to aggregate costs.

- The Definition: A specific customer order or a distinct “batch” of production that is clearly distinguishable from other products or services.

- The Core Logic: Each Job consumes a unique combination of resources—different materials, specialized labor hours, and varying levels of technical expertise.

- Representative Examples:

- Construction: “The structural renovation of a specific luxury hotel wing.”

- Professional Services: “A specialized legal defense strategy for a corporate merger.”

- Manufacturing: “The production of a custom-engineered satellite for a telecommunications firm.”

- Creative Industry: “The development of a high-budget cinematic production for a global streaming platform.”

2. Defining Job Order Costing and Its Core Characteristics

Job Order Costing is the go-to system when products differ so significantly in specifications, quality, and design that their costs must be tracked individually.

- Functional Definition: A method where costs are accumulated separately for each specific job. The total manufacturing cost is only finalized once that specific project is completed.

- Target Industries: Best suited for high-variety, low-volume production or custom-order business models (e.g., Shipbuilding, Aerospace, Construction, High-end Printing, Specialized Accounting, and Advertising).

- The Strategic Advantage: It allows for a microscopic analysis of profit and cost per product, which is vital for precise pricing and long-term profitability management.

- The Operational Challenge: Because every resource must be traced to a specific job, it involves extensive documentation and higher administrative overhead.

- The Calculation Framework: Total Manufacturing Cost = Direct Materials + Direct Labor + Manufacturing Overhead

3. The Flow of Value: The Job Cost Sheet

The “heart” of Job Order Costing is the Job Cost Sheet. Think of this as the financial diary for a specific project, recording every resource sacrifice made to bring the project to life.

| Component | Description | Nature |

| Direct Materials | Recorded based on raw material requisitions specifically pulled for that job. | Directly Traceable |

| Direct Labor | Tracked via Time Tickets filled out by specialists for the exact hours spent on the job. | Directly Traceable |

| Manufacturing Overhead | Common costs (rent, utilities, depreciation) shared across various jobs. | Requires Allocation |

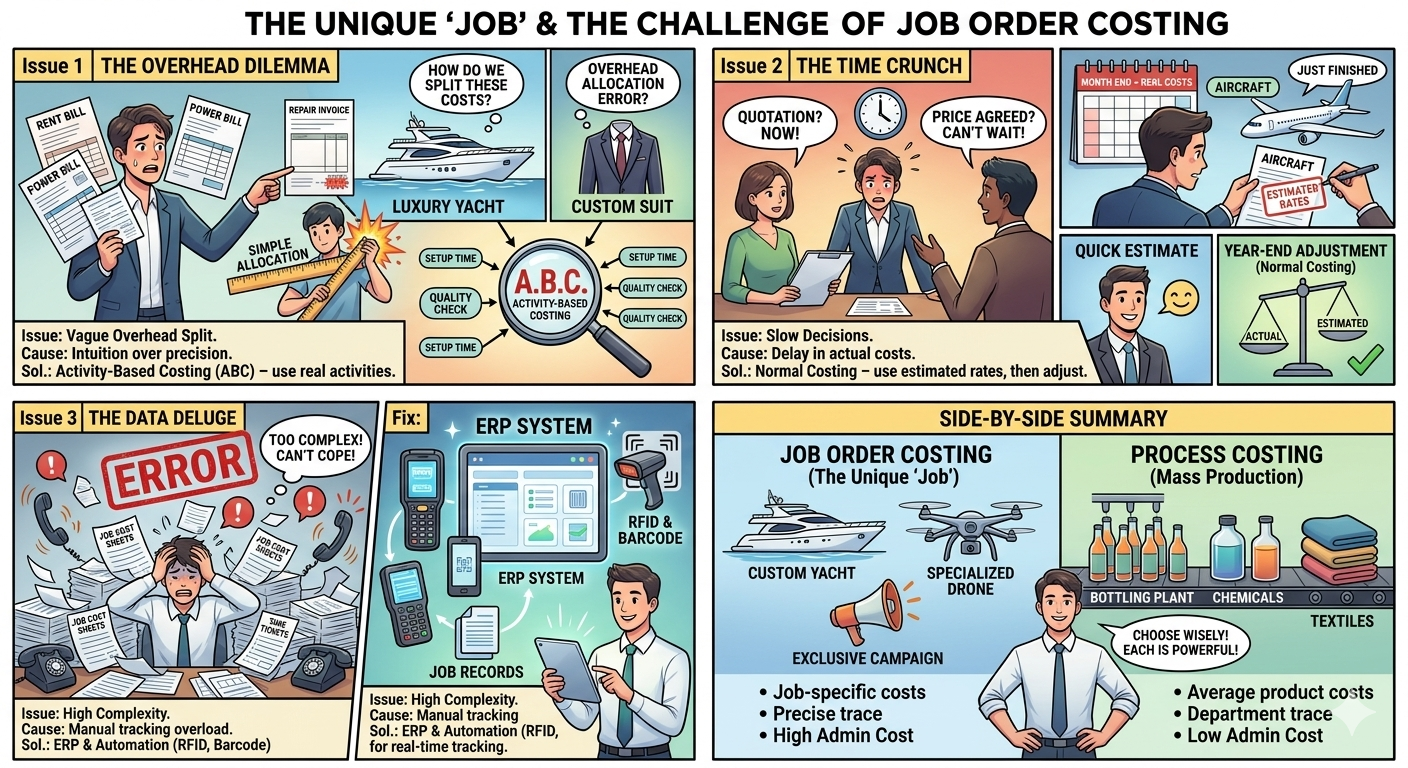

4. Major Strategic Issues in Job Order Costing

Implementing Job Order Costing is essential for custom-driven businesses, but its microscopic nature presents several sophisticated challenges. Here is how modern enterprises address them.

1) The Precision of Manufacturing Overhead Allocation

The most classic dilemma is how to fairly distribute “shared costs” like rent or electricity among different projects.

- The Root Cause: Unlike direct materials, you cannot physically see how much electricity was “consumed” by a specific custom-made part. An arbitrary allocation often leads to distorted profit figures.

- The Modern Solution: Moving toward Activity-Based Costing (ABC). Instead of using a broad metric like “total labor hours,” costs are allocated based on specific activities (e.g., number of machine setups or inspection hours) that actually drive the cost.

- The Strategic Result: This eliminates “hidden” resource drain and ensures that high-maintenance projects pay their fair share.

2) Information Timeliness and the “Normal Costing” Adjustment

In a fast-paced market, a manager cannot wait until the end of the fiscal year to set a price.

- The Root Cause: Actual overhead costs (like fluctuating utility bills) are often only finalized at month-end or year-end, but pricing and quotes must be delivered the moment a project starts.

- The Modern Solution: Utilizing Normal Costing. Companies establish a “Predetermined Overhead Rate” based on historical data to estimate costs in real-time. Any variance between the estimate and reality is adjusted during the final closing.

- The Strategic Result: This enables agile decision-making and allows the firm to respond to market shifts with accurate, data-backed quotes.

3) Complexity and the Burden of Administrative Cost

Tracking every minute and every bolt for every project creates a massive amount of data.

- The Root Cause: Managing individual Job Cost Sheets for hundreds of projects increases the risk of data entry errors and administrative fatigue.

- The Modern Solution: Integrating ERP (Enterprise Resource Planning) systems with automation tools like Barcodes, RFID, and automated time-tracking software.

- The Strategic Result: This secures the reliability of data and allows the finance team to shift from “data entry” to “strategic analysis.”

5. Global Comparison: Job Order vs. Process Costing

The choice of costing system defines your entire business architecture.

| Feature | Job Order Costing | Process Costing |

| Production Logic | High Variety, Low Volume / Custom | Low Variety, High Volume / Continuous |

| Cost Aggregation | By Individual Job | By Department or Process |

| Key Document | Job Cost Sheet | Production Cost Report |

| Typical Industry | Specialized Engineering, Luxury Goods | Oil Refining, Chemicals, Staples |

6. The Strategic Frontier: Manufacturing Cost vs. Total Cost

A common pitfall in Job Order Costing is failing to distinguish between official reporting and strategic reality.

1) The Regulatory Lens: Strict Manufacturing Focus

Under U.S. GAAP or IFRS, Selling, General, and Administrative (SG&A) expenses are strictly excluded from product cost.

- The Nature: These are “Period Costs.”

- The Logic: They are expensed immediately and never “sit” in inventory. Only the costs incurred within the “four walls” of the factory are recognized as assets.

2) The Management Lens: Finding True Profitability

For a CEO, the regulatory definition is often insufficient. To find the “True Profit,” one must track SG&A costs directly to specific projects. This is called Customer Profitability Analysis.

- The Scenario: Project A and Project B both have a manufacturing cost of $1M. However, Project A required $200k in specialized international shipping and dedicated marketing.

- The Strategic Insight: On the official balance sheet, they look identical. In reality, Project B is much more profitable. Without tracking these “hidden” non-manufacturing costs to the specific Job, a company risks over-investing in high-maintenance, low-margin clients.

7. Conclusion: Why the Job Order Perspective Matters

Job Order Costing is far more than a clerical task. It is a strategic diagnostic tool that answers two of the most critical questions in any enterprise: “Which specific project is truly driving our wealth?” and “What is our real margin when we agree to a custom order?”

By mastering the allocation of “invisible” overhead while meticulously tracking “visible” direct costs, a manager moves from guessing to knowing. This is where the true competitive advantage is born.

Conclusion: Key Takeaways

- Precision is Power: Job Order Costing turns “estimates” into “intelligence” by treating every project as a unique financial entity.

- Strategic Allocation: The success of the system depends on how logically you allocate the “untraceable” overhead.

- Beyond the Factory: For a leader, “Cost” should include all resources—even marketing and shipping—to see the true profitability of a client.

AI Disclosure: Created in collaboration with Google Gemini. All core content was authored, reviewed, and edited by the author.