We have previously explored the overall mechanism of Job Order Costing and the critical role of the “Job Cost Sheet.” While Direct Materials and Direct Labor are relatively straightforward to track to a specific Job, the real headache for a CEO lies in Common Costs—specifically, how to fairly distribute Manufacturing Overhead (MOH).

Costs like factory rent, depreciation of expensive machinery, and shared utility bills do not leave a direct trail to a single product. Today, we will deconstruct the principle of Overhead Allocation, the core factor that determines the accuracy of your financial intelligence.

1. What is Overhead Allocation?

Allocation is the process of assigning common costs that cannot be directly traced to a specific job or product by using a rational benchmark known as a Cost Driver.

In Job Order Costing, direct costs are easy to pin down. However, because Manufacturing Overhead—such as rent for a massive Amazon Fulfillment Center or the depreciation of a Tesla Giga-press—is incurred for multiple product lines simultaneously, a logical “distribution” process is mandatory.

- The Core Objective: To calculate a product cost that most closely reflects the “actual resource consumption” of each job.

- The Cost Driver: You must select a factor with a high cause-and-effect relationship. For example, in a machine-heavy automated plant, Machine Hours is the ideal driver; in a high-touch manual assembly line, Direct Labor Hours is more appropriate.

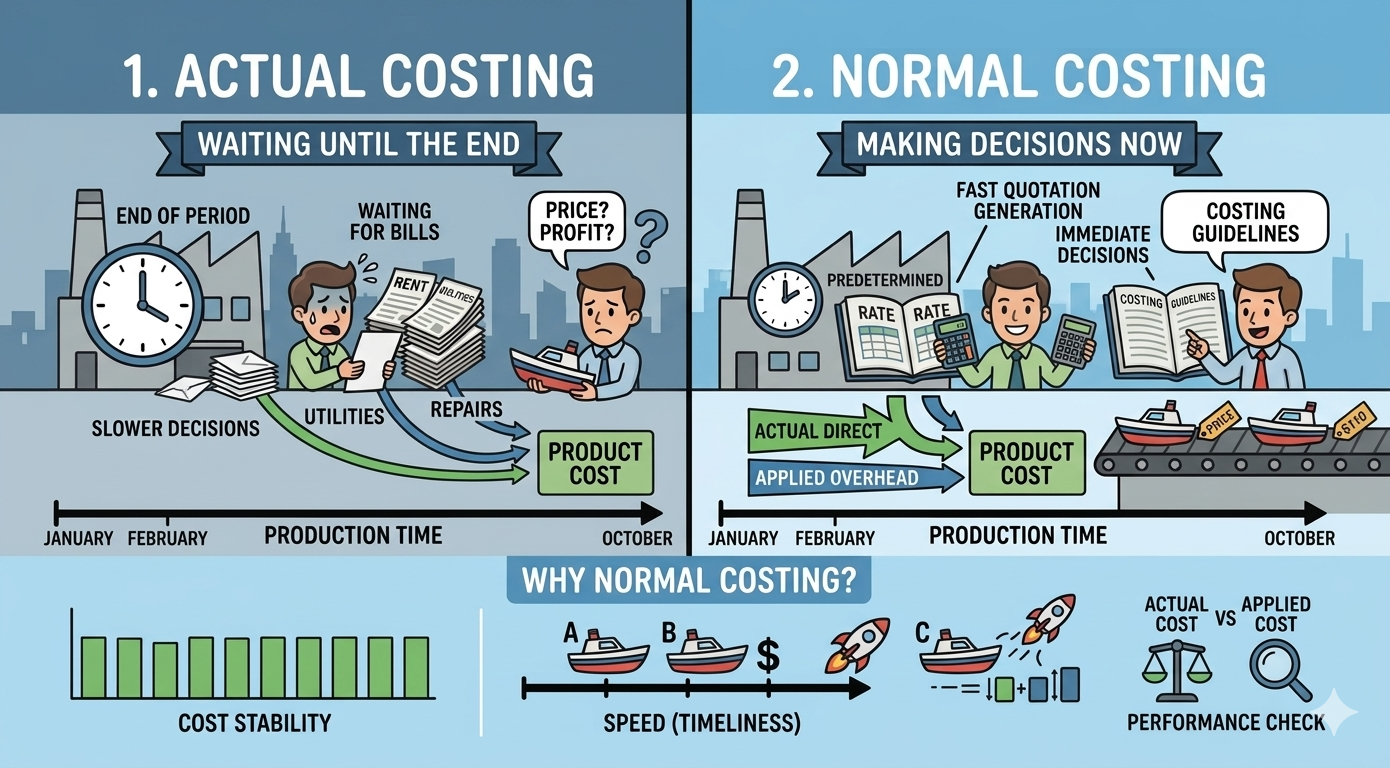

2. Actual Costing vs. Normal Costing

The timing of when you finalize and allocate overhead determines the speed of your business decisions.

1) Actual Costing

This method allocates the total overhead only after the actual costs are finalized at the end of the fiscal period. While the numbers are “accurate,” you have to wait until the end of the month or year. This makes it nearly impossible to set prices or analyze profitability immediately after a job is finished.

2) Normal Costing: The Executive’s Choice

This is the preferred method in the real business world. While direct costs (materials and labor) are recorded at their actual amounts, Manufacturing Overhead is applied using a “Predetermined Overhead Rate (POHR)” set at the beginning of the year. This allows for rapid quoting and real-time decision-making.

3. Why Normal Costing? “Delayed Information is No Information”

1) The Limits of Actual Costing

Imagine you are dining at a high-end steakhouse in Manhattan. When you ask for the check, the owner says, “Well, our electricity and water bills won’t arrive until next month, so I’ll let you know the price of your steak then.” This is exactly the problem with Actual Costing.

- Lack of Timeliness: Real overhead costs (rent, power, repairs) are often finalized long after a product is completed. A manager needs to know the cost immediately to set a competitive price.

- Cost Volatility: Actual costs fluctuate due to seasonal factors. A product made in a scorching August (with high AC costs) might appear more “expensive” than the same product made in October, creating a Cost Distortion.

2) The Rise of Normal Costing: Predictive Decision-Making

Normal Costing was designed to fix these weaknesses by using a bridge of rational estimation.

- Definition: Recording actual direct costs but applying overhead based on a rate established at the start of the year.

- The Strategic Benefits:

- Rapid Quoting: Enables real-time cost estimation even while production is ongoing.

- Cost Smoothing: Stabilizes the unit cost by removing temporary fluctuations (like a one-time spike in utility rates).

- Performance Benchmarking: Since you have a “predetermined” standard, you can later compare it to reality to ask: “Why did our actual costs exceed our forecast?”

4. Calculating the Rate: Predetermined vs. Actual

| Feature | Predetermined Overhead Rate (POHR) | Actual Overhead Rate |

| Calculation Timing | Beginning of the Period (Forecast) | End of the Period (Finalized) |

| The Formula | Budgeted Overhead / Estimated Activity | Actual Overhead / Actual Activity |

| Primary Advantage | Provides immediate, real-time data | Matches actual historical expenditures |

| Primary Disadvantage | Requires year-end variance adjustment | Information is too slow for decision-making |

5. The Mechanism of Predetermined Overhead Application

The accuracy of Job Order Costing depends on how logically you assign overhead. Here is the mechanism used by global enterprises.

1) The Calculation Formula

Before the fiscal year begins, the POHR is calculated based on historical data and future forecasts:

POHR = Total Estimated Overhead Costs / Total Estimated Activity Base (e.g., Labor Hours)

Then, the amount Applied to a specific product is determined by:

Applied Overhead = POHR × Actual Activity used for that Job

2) Critical Considerations for Implementation

- Appropriateness of the Cost Driver: If your plant is automated, using labor hours as a driver will distort your data. You must use machine hours.

- Activity Levels: Use “Normal Capacity” (what is realistically achievable) rather than “Theoretical Maximum” to keep the cost data grounded in reality.

- External Factors: Budgets must account for inflation, rising energy costs (e.g., a spike in natural gas prices), or changes in lease agreements to minimize year-end gaps.

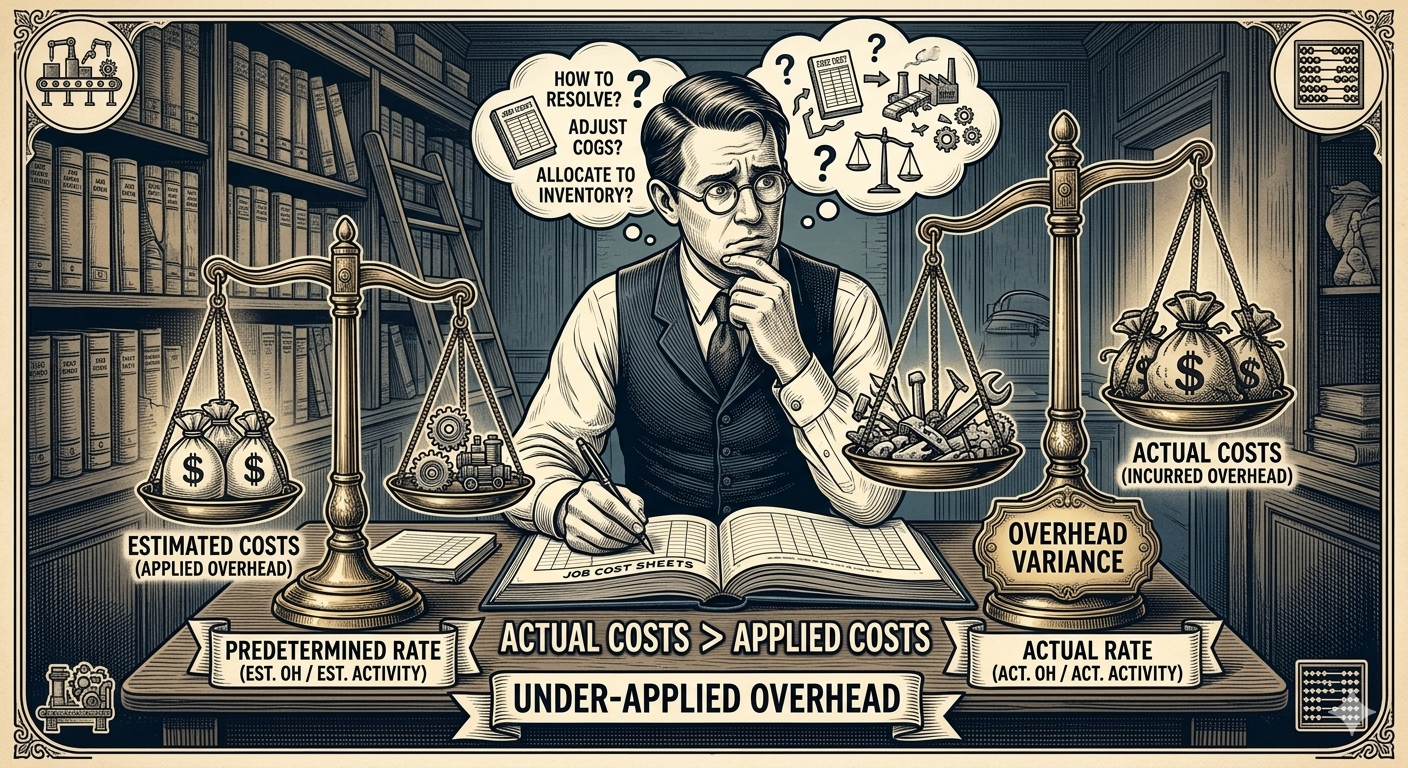

6. Understanding the Gap: Under-applied vs. Over-applied

At the end of the year, there will inevitably be a difference between the “Applied” (estimated) overhead and the “Actual” overhead. This is the Overhead Variance.

- Under-applied Overhead: (Actual Costs > Applied Costs)You estimated your costs too low. This usually means your actual expenses were higher than your plan, requiring an adjustment that decreases net income at year-end.

- Over-applied Overhead: (Actual Costs < Applied Costs)You were too conservative and estimated costs too high. This results in an adjustment that increases net income at year-end.

The Management Compass: A variance isn’t just an accounting entry; it’s a signal. It tells a leader whether the gap was caused by a flawed forecast (Budgeting error) or operational inefficiency on the floor (Waste).

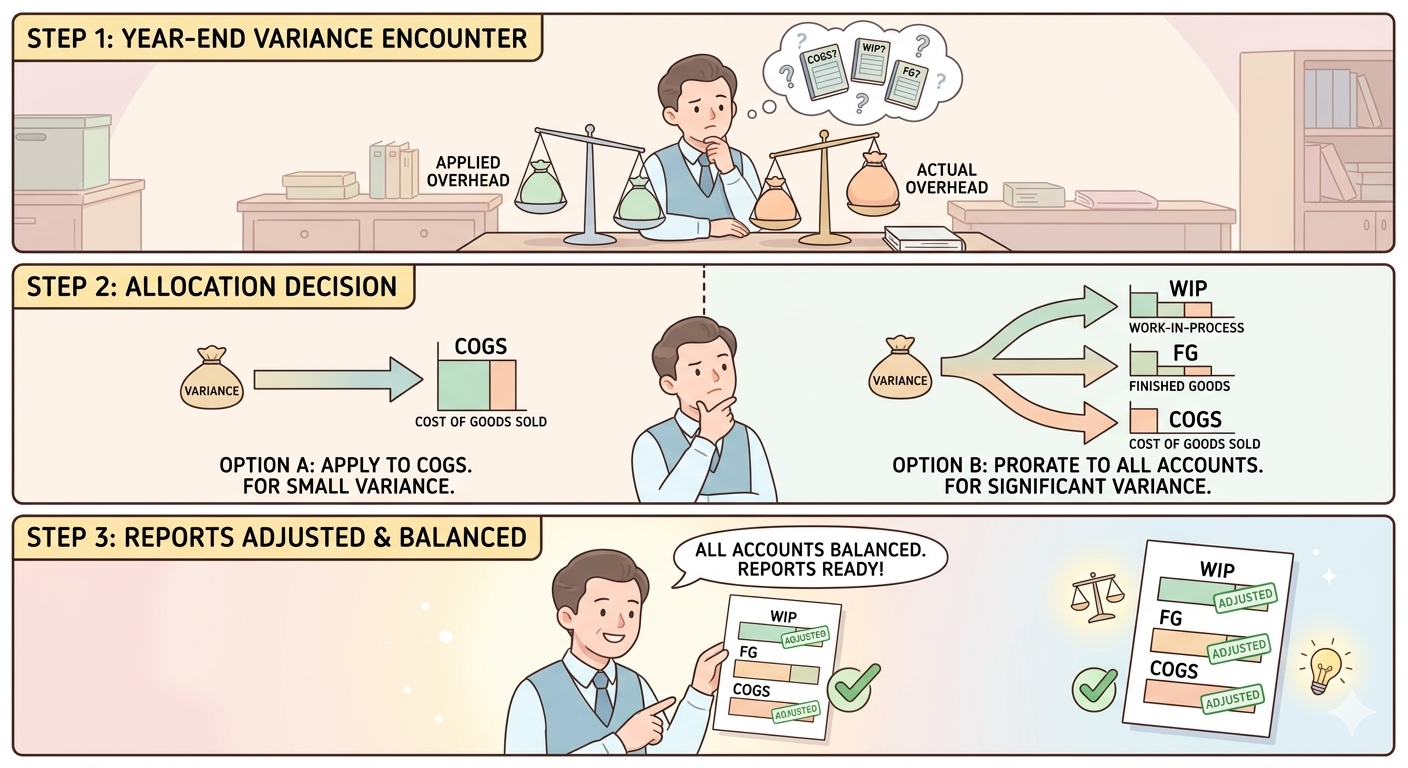

7. Year-End Treatment of Variances

According to financial regulations (U.S. GAAP/IFRS), these variances must be adjusted to reflect the actual costs incurred.

- Cost of Goods Sold (COGS) Method: The entire variance is closed out to COGS. This is simple and used when the amount is immaterial (not large enough to distort the big picture).

- Proration Method: The variance is distributed proportionally among Work-in-Process (WIP), Finished Goods, and COGS based on their relative balances. This is used when the amount is significant and requires a high degree of reporting accuracy.

- Prorate : To distribute a cost variance proportionally across different accounts so that each reflects its fair share of the actual cost.

8. Conclusion: The Strategic Value of Normal Costing

Normal Costing is not just about “guessing.” It is a strategic forecasting tool that smooths out the noise of seasonal spikes and provides a consistent “Floor” for your pricing strategy. By understanding the gap between your Applied costs and Actual costs, you gain a powerful navigation tool to correct your course for the next fiscal year.

Conclusion: Key Takeaways

- Timeliness over Perfection: Normal Costing prioritizes giving managers data now so they can win contracts and set prices.

- Drivers Must Reflect Reality: Choosing the wrong Cost Driver (e.g., using labor hours in an AI-driven factory) is the fastest way to distort your profit data.

- Variance as a Signal: Under-applied or Over-applied overhead is a report card on your strategic planning. Analyze it to sharpen your next move.

AI Disclosure: Created in collaboration with Google Gemini. All core content was authored, reviewed, and edited by the author.