If you want to avoid the high volatility of the stock market but find the low returns of traditional bank savings accounts or Certificates of Deposit disappointing, bonds may very well emerge as the absolute protagonist of the financial market in the second half of 2026. As the high interest rates observed as of June begin their full-fledged downward cycle in the latter half of the year, bonds—which were once considered the exclusive playground of giant institutional players—are firmly establishing themselves as an essential portfolio asset for individual retail investors. In this post, we reveal the 2026 bond investment trends chosen by smart investors aiming to capture both tax efficiency and capital gains simultaneously in the global capital markets.

1. What is a Bond? A Formal IOU from Governments and Corporations

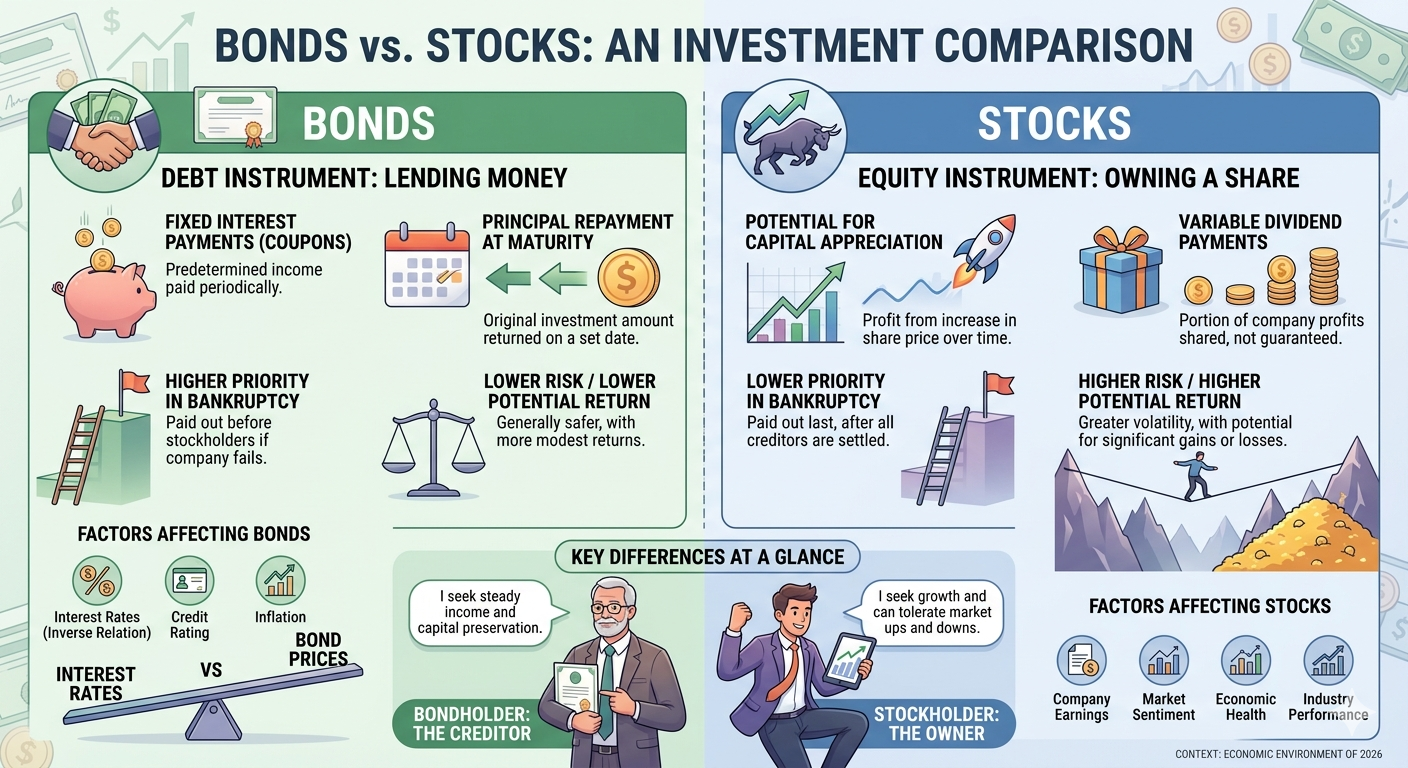

Bond investment is not overly complicated. To put it simply, it is a type of financial certificate where you lend money to a sovereign government or a corporation, and in return, you receive fixed interest payments alongside the structural rights stipulated by that security.

To use an everyday analogy, it is just like lending money to a friend and writing a formal IOU agreement. The borrower promises, “I will borrow this specific amount of capital from you. In return, I will pay you a fixed interest rate on a regular basis, and when the promised maturity date arrives, I will return your initial principal in full.” The only difference in the financial markets is that the entities borrowing your money are incredibly reliable institutions, such as the US Treasury or blue-chip corporations.

2. The Mechanics of Price: The Seesaw Relationship with Interest Rates

The market price of a bond fluctuates every single day, and the absolute dominant factor driving this movement is the prevailing market interest rate. The most fundamental rule you must memorize in bond investing is that when interest rates fall, bond prices rise.

To understand the core principle, imagine you currently hold an older bond that locks in a fixed 5% annual coupon rate. If the Federal Reserve suddenly cuts benchmark rates and the general market interest rate drops to 3% for new securities, your existing bond instantly becomes highly valuable. Since your bond pays an interest rate that is 2% higher than what anyone can get from newly issued bonds, investors will line up and compete to buy your security on the secondary market. This surges the demand and drives your bond’s price upward. Market interest rates and bond prices sit on exact opposite ends of a macroeconomic seesaw—when one goes down, the other must go up.

3. The 2026 Macro Environment: Stock Market Milestones and the Easing Cycle

As of June 2026, the US stock market has experienced significant upward momentum, driven heavily by booms in core sectors like artificial intelligence and semiconductors, leading major indices to hit historic milestones. Globally, even amidst geopolitical tensions and macroeconomic shifts that have kept the US Dollar Index remarkably strong and interest rates stubbornly elevated, a structural shift is on the horizon. As these geopolitical conflicts show signs of cooling down and moving toward stability, global economic growth is expected to moderate.

Consequently, inflation will stabilize back toward the Federal Reserve’s target levels of 2%, and interest rates will enter a long-term downward stabilization phase. As the Federal Reserve paves the way for a clear cycle of benchmark fed funds rate cuts, a major wealth-generation window is opening up—allowing individual retail investors to capture massive capital gains before institutional capital completely floods the market.

4. Decoding Similar Financial Products

While bonds share similarities with other income-generating vehicles, their structural differences are distinct:

- Fixed Deposits vs. Bonds: Traditional bank fixed savings accounts or CDs lock your money away for a set term. While bonds also offer predictable income, they can be traded freely on the secondary open market prior to maturity, allowing investors to exit early or capture immediate capital gains.

- Commercial Paper / Banker’s Acceptances vs. Bonds: These are short-term corporate debt instruments issued by financial institutions. They offer fixed short-term yields but lack the long-duration capital appreciation potential of long-term bonds during a rate-cut cycle.

- Real Estate Investment Trusts (REITs) vs. Bonds: REITs pass regular rental income to investors in the form of dividends, mimicking a bond’s coupon. However, REITs carry much higher underlying equity risk, meaning their capital preservation security is fundamentally lower than that of high-grade government bonds.

5. The Two Engines of Bond Returns

Active market capital generates wealth through bonds using two entirely distinct investment mechanisms:

- Coupon Yield: This is the predictable cash flow generated by holding the bond and collecting the locked-in, contractual interest payments. Investors who buy high-quality, investment-grade corporate bonds and hold them all the way to maturity use this engine to lock in cash flow yields superior to traditional bank accounts.

- Capital Gains: This is the strategic profit generated by selling the bond at a higher price than your purchase price on the secondary market before it matures. Aggressive traders use this engine to capture massive windfalls by calculating the velocity of falling market interest rates and riding the corresponding spike in bond values.

6. Bonds vs. Stocks: A Comprehensive Structural Comparison

Because these two asset classes possess opposite characteristics, combining them is the ultimate way to optimize and balance an investment portfolio.

| Category | Bonds | Stocks |

| Investor Status | Creditor (A lender holding senior debt claims) | Shareholder (A fractional owner of the corporation) |

| Source of Return | Contractual Coupons + Capital Gains | Market Price Appreciation + Discretionary Dividends |

| Income Structure | Highly Predictable (Contractually Fixed) | Inherently Uncertain (Tied to Corporate Performance) |

| Risk Level | Low to Moderate (Backed by Issuer Credit) | High (Potential for Complete Loss of Principal) |

| Macro Environment | Outperforms during Easing & Rate-Cut Cycles | Outperforms during Economic Growth & Booms |

| Portfolio Role | The Strategic Defensive Shield / Safety Net | The Aggressive Growth Engine / Attacking Force |

7. How Individual Investors Access the Fixed Income Market

In 2026, individual retail investors no longer face the high institutional barriers of the past. You can easily build a fixed-income portfolio through several user-friendly avenues:

- Brokerage Apps (MTS): Modern mobile trading platforms allow individual retail investors to scan, analyze, and purchase US Treasury bills, notes, or individual investment-grade corporate bonds as simply as buying retail products online.

- Bond ETFs: These are diversified baskets of bonds that trade in real time on stock exchanges. Because you can buy or sell them instantly for a low price of around $10 to $100 per share, they represent the most popular and liquid vehicle for retail capital allocation.

- Specialized Treasury Portals: Setting up dedicated direct accounts allows individual retail investors to buy long-term government debt directly, maximizing compound interest advantages over extended horizons.

- Tax-Advantaged Accounts (Traditional/Roth IRAs & 401(k)s): Allocating fixed-income assets or bond ETFs inside tax-sheltered retirement structures is the ultimate standard practice. It allows investors to completely defer or eliminate ordinary income taxation on coupons, drastically increasing net wealth compounding.

8. Mastering the Timing: When to Accumulate and When to Liquidate

The ultimate success of your fixed-income strategy relies entirely on correctly mapping out the trajectory of interest rates.

- The Buying Window (Accumulation): The absolute ideal entry point occurs when macroeconomic indicators show that central bank interest rates have reached their peak and are poised to enter a downward cycle. Purchasing long-duration assets at this structural bottom ensures you lock in high yields and position your portfolio for maximum capital gains as rates drop.

- The Selling Window (Execution): Once interest rates have fully bottomed out and bond prices have peaked, or if macro data flashes warnings of renewed inflation that could force rates back up, smart investors liquidate their positions to lock in their capital gains. If rates face upward pressure, transitioning to a defensive holding strategy to collect fixed coupons until maturity is the safest course of action.

9. Utilizing Bond Funds and Institutional Management

For individuals who prefer not to manage individual debt maturities, professionally managed fixed-income funds offer an excellent structural alternative.

- What is a Bond Fund? It is a pooled investment vehicle where institutional fund managers collect retail capital and systematically deploy it across a vast, diversified matrix of government and corporate debt.

- Core Advantages: They grant retail investors instant diversification across hundreds of institutional-grade securities with minimal capital, effectively mitigating idiosyncratic default risk. Furthermore, professional management actively rebalances duration exposure based on real-time Federal Reserve dot plots and macroeconomic shifts.

- Key Varieties: Investors can choose among highly secure Sovereign Treasury Funds, yield-maximizing High-Yield / Junk Bond Funds, or highly liquid, exchange-traded Treasury ETFs depending on their specific risk tolerance.

Conclusion: Key Takeaways for Today’s Investors

Bonds are far from a boring, stagnant investment; rather, they represent one of the most scientific, predictable methods of converting the macroeconomic passage of time and central bank policy into structured portfolio returns.

- Mastering the Timing: Understand the difference between the 2026 bottoming and the 2027 easing. The second half of 2026 represents the accumulation phase where smart retail investors buy the rumor of rate cuts. Early 2027 will likely be the execution phase where consecutive rate cuts materialize into clear capital appreciation.

- Shield Your Returns: For those actively designing a retirement timeline, channeling fixed-income assets through tax-deferred vehicles like IRAs or 401(k) accounts is the ultimate alpha strategy to secure both safety and tax minimization in 2026.

- Watch Macro Signals: Pay close attention to Federal Reserve dot plots, labor market data, and central bank communication regarding inflation targets. The velocity of the upcoming interest rate cuts will dictate exactly how fast your long-term bond prices will appreciate.

AI Disclosure: Created in collaboration with Google Gemini. All core content was authored, reviewed, and edited by the author.